Kevin Warsh is changing the way the Federal Reserve speaks to markets.

At the ECB’s annual Forum on Central Banking in Sintra, Portugal, the new Fed Chair made one message clear. Inflation risks may have eased in recent weeks, but the Fed is not ready to declare victory.

That matters because markets have been looking for signs that lower oil prices and progress in US-Iran peace negotiations could soften the Fed’s stance. The Middle East energy shock has started to reverse, shipping through the Strait of Hormuz has improved, and oil prices have fallen from the extremes seen during the conflict.

But Warsh is not treating lower oil as a reason to relax.

He is treating it as one input in a much bigger inflation fight.

The Fed’s preferred inflation gauge remains far above target. Headline PCE inflation recently accelerated to 4.1%, while core PCE rose to 3.4%. Both readings remain well above the central bank’s 2% objective and support the Fed’s decision last month to raise its inflation forecasts sharply.

That is why Warsh’s tone remains firm.

He emphasized that price stability is still the Fed’s primary objective. This is important because inflation is no longer just an energy story. Services inflation remains sticky, labour demand is still resilient, and the economy has not weakened enough to justify a softer policy stance.

The labour market is central to this debate.

Recent JOLTS data showed job openings climbing to a two-year high, while markets are expecting another solid nonfarm payrolls report. If jobs remain strong while inflation stays elevated, the Fed has room to keep policy restrictive or even raise rates again later this year.

That is the market’s concern.

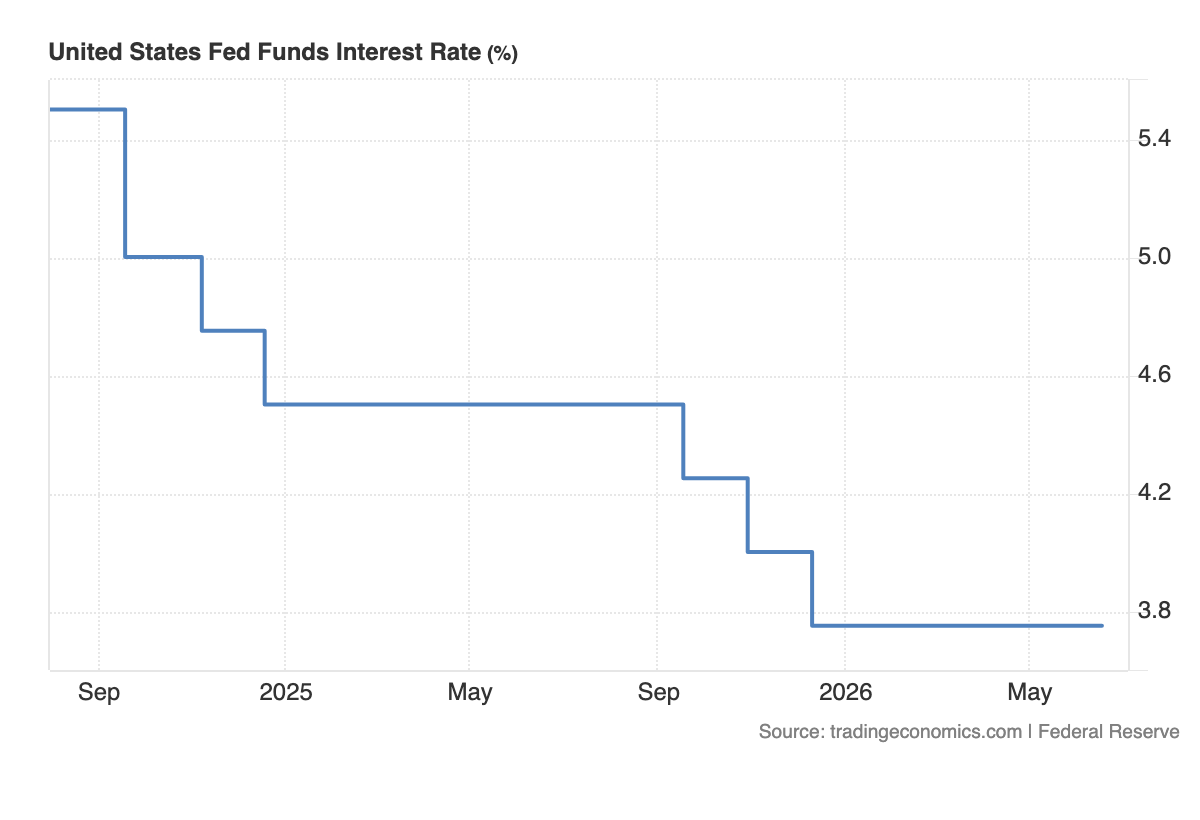

Last month, the Fed held rates steady at 3.50% to 3.75%, but the projections showed growing support for additional tightening. Roughly half of policymakers now expect at least one rate hike this year, with some officials expecting more than one.

Warsh did not push back against that risk.

Instead, he declined to comment on the upcoming policy decision and said the Fed will base its choices on incoming data. That may sound neutral, but it is not dovish. It means markets will no longer get comfort from predictable forward guidance.

This is a major shift.

For years, investors became used to central banks guiding expectations in advance. Markets wanted hints, timelines and signals. Warsh is moving in the opposite direction. He is telling investors that the Fed will not pre-commit.

That increases the importance of every major data release.

PCE, CPI, payrolls, wages, retail sales and job openings now carry more weight because the Fed is no longer smoothing the path for markets with clear guidance. If inflation stays hot, the market has to price hikes. If labour weakens sharply, the market can price caution. But the Fed will not give investors the answer in advance.

This is also why Warsh emphasized independence.

His comments dismissing political pressure were not just institutional language. They were a signal that the Fed wants to protect its credibility after a period of high inflation, energy-market disruption and political pressure over rates.

That credibility matters for the dollar.

If markets believe the Fed is serious about restoring price stability, US yields stay supported. Higher yields increase the appeal of dollar assets and help explain why the dollar has remained strong even as geopolitical risks have eased.

Gold faces the opposite problem.

Lower oil and progress in peace talks should theoretically help gold by reducing inflation pressure and lowering future rate expectations. But that has not been enough because the Fed’s reaction function remains hawkish. As long as yields stay high and the dollar remains firm, gold rallies are likely to remain fragile.

Equities also face a more complicated environment.

Lower oil supports margins and consumer spending, but a Fed that refuses to guide markets toward easier policy keeps valuation pressure alive. Growth stocks, especially AI and technology names, are more vulnerable when yields remain elevated and policy uncertainty rises.

This is the real message from Sintra.

Warsh is not saying inflation risks are gone.

He is saying the Fed will keep adapting its strategy until inflation is back at target.

That means lower oil alone will not be enough to change the policy outlook. The Fed needs evidence that inflation is cooling across the broader economy, especially in services and core prices.

For markets, the takeaway is clear.

The Fed is becoming less predictable by design.

It is moving away from forward guidance, defending its independence and forcing investors to focus on the data.

That makes the next phase of the market cycle more volatile.

The inflation shock may be easing.

But the Fed’s inflation fight is not over.