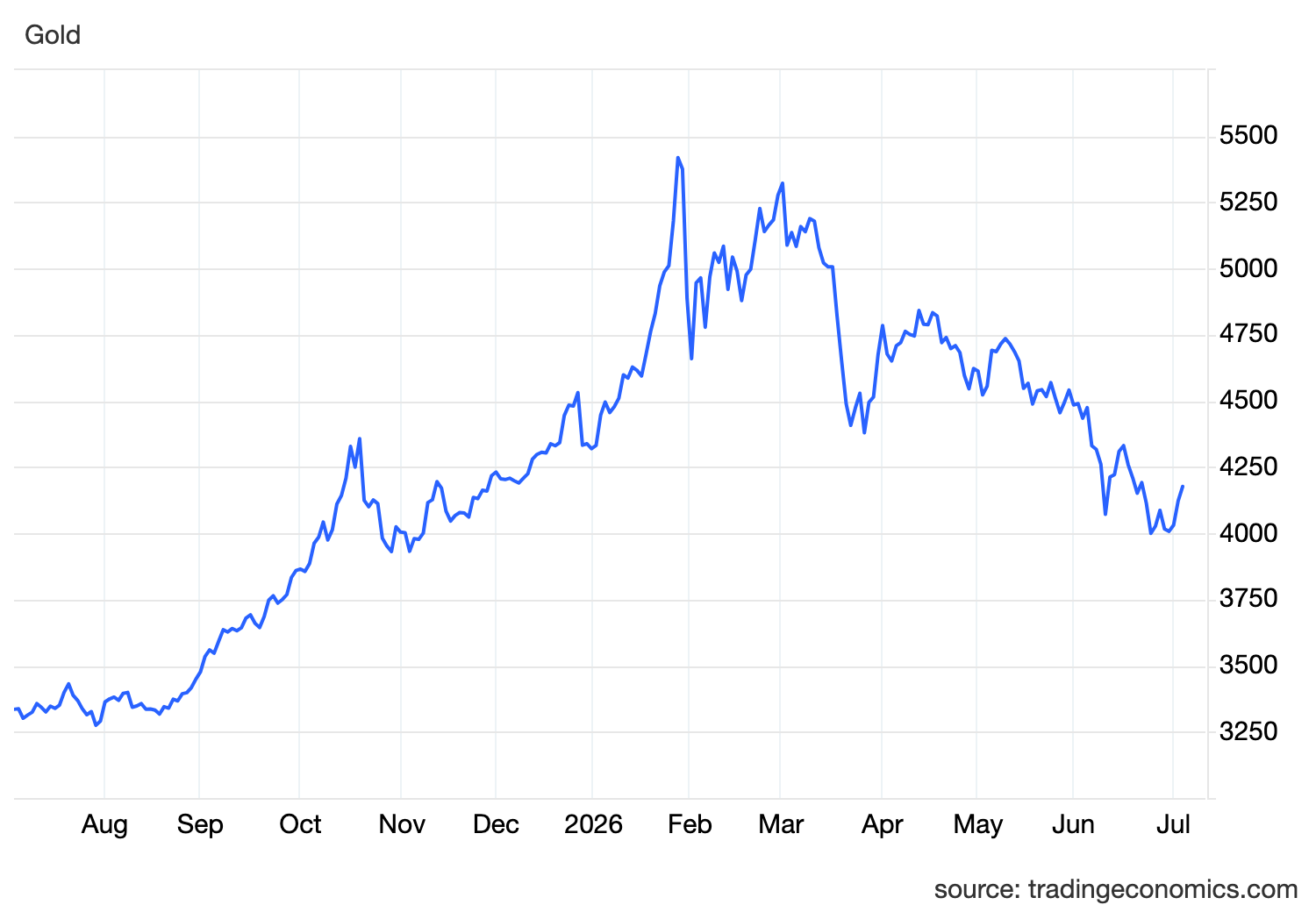

Gold finally got the relief it needed.

The metal climbed toward $4,200 after weaker-than-expected US employment data forced traders to scale back expectations for Federal Reserve rate hikes. After weeks of pressure from sticky inflation, a firm dollar and elevated Treasury yields, the latest jobs report gave markets a reason to question whether the Fed can tighten policy as aggressively as previously priced.

The US economy added just 57,000 jobs in June, far below expectations of 110,000 and the weakest increase in four months. The unemployment rate held at 4.2%, but the headline payroll figure was soft enough to shift the market conversation.

That matters directly for gold.

Gold does not pay interest, so it struggles when investors expect higher rates. When Fed hike expectations rise, Treasury yields tend to stay supported, the dollar strengthens and bullion becomes less attractive relative to cash and bonds.

This time, the opposite happened.

Fed funds futures now imply roughly a 50% chance of a September rate hike, down from 67% before the jobs report. That reduction in rate hike expectations lowered the pressure on gold and allowed buyers to return.

The move also followed weaker private-sector employment data earlier in the week, reinforcing the idea that the labour market may finally be losing momentum.

This is important because the Fed’s policy dilemma has been built around two forces.

Inflation has remained too high.

But growth and jobs had stayed strong enough to give policymakers room to remain hawkish.

The latest employment data weakens that second pillar.

If the labour market continues to cool, the Fed may find it harder to justify another rate hike, even with inflation still above target. That is why gold reacted positively. The market is not saying inflation has been solved. It is saying the Fed may have less room to tighten if jobs continue slowing.

Kevin Warsh’s recent comments also helped the shift.

The Fed Chair said inflation expectations are moderating, while still reaffirming the central bank’s commitment to price stability. That balance matters. Warsh is not turning dovish, but he is acknowledging that some inflation risks have eased.

That is where oil becomes important.

The recovery of commercial shipping through the Strait of Hormuz and progress in US-Iran talks have helped push oil prices lower. Lower oil reduces the risk of a fresh energy-driven inflation shock, which had been one of the main reasons markets were pricing additional Fed tightening earlier this year.

This is the same macro chain that has driven markets for months.

The Middle East conflict disrupted oil supply.

Higher oil pushed inflation higher.

Higher inflation lifted Treasury yields.

Higher yields supported the dollar.

A stronger dollar and higher yields pressured gold.

Now parts of that chain are beginning to reverse.

Hormuz shipping is recovering. Oil prices are lower. Inflation expectations are easing. Labour data is softening. Rate hike bets are falling. That combination gives gold room to recover.

Still, the rebound should not be treated as a full trend reversal yet.

Core inflation remains above the Fed’s 2% target, and the latest PCE data showed price pressures are still sticky. Services inflation remains particularly important because it tends to be more persistent than energy inflation.

That means the Fed is unlikely to declare victory quickly.

Policymakers will need more than one weak jobs report and lower oil prices before shifting away from their inflation-fighting stance. The Fed will want evidence that wage pressure is cooling, services inflation is easing and demand is slowing in a controlled way.

This makes the next few data releases critical.

If CPI, PCE and wage data soften alongside weaker employment, gold could extend its recovery as yields fall and the dollar loses momentum. In that scenario, markets would likely reduce expectations for a September rate hike even further.

But if inflation remains firm while the labour market stabilizes, the Fed’s hawkish stance could quickly return.

That would put gold back under pressure.

For now, however, the market has shifted from fear of aggressive Fed tightening to hope that policy may become more balanced.

Gold is rising because the rate story has softened.

Not because the inflation fight is over.

Not because geopolitical risk has disappeared.

But because weaker jobs, lower oil and easing inflation expectations have reduced the pressure that had been weighing on bullion.

The key takeaway is simple.

Gold needed a break in the Fed story.

The jobs report delivered it.