US inflation is back above 4%, and this is exactly the kind of report that keeps the Federal Reserve boxed in.

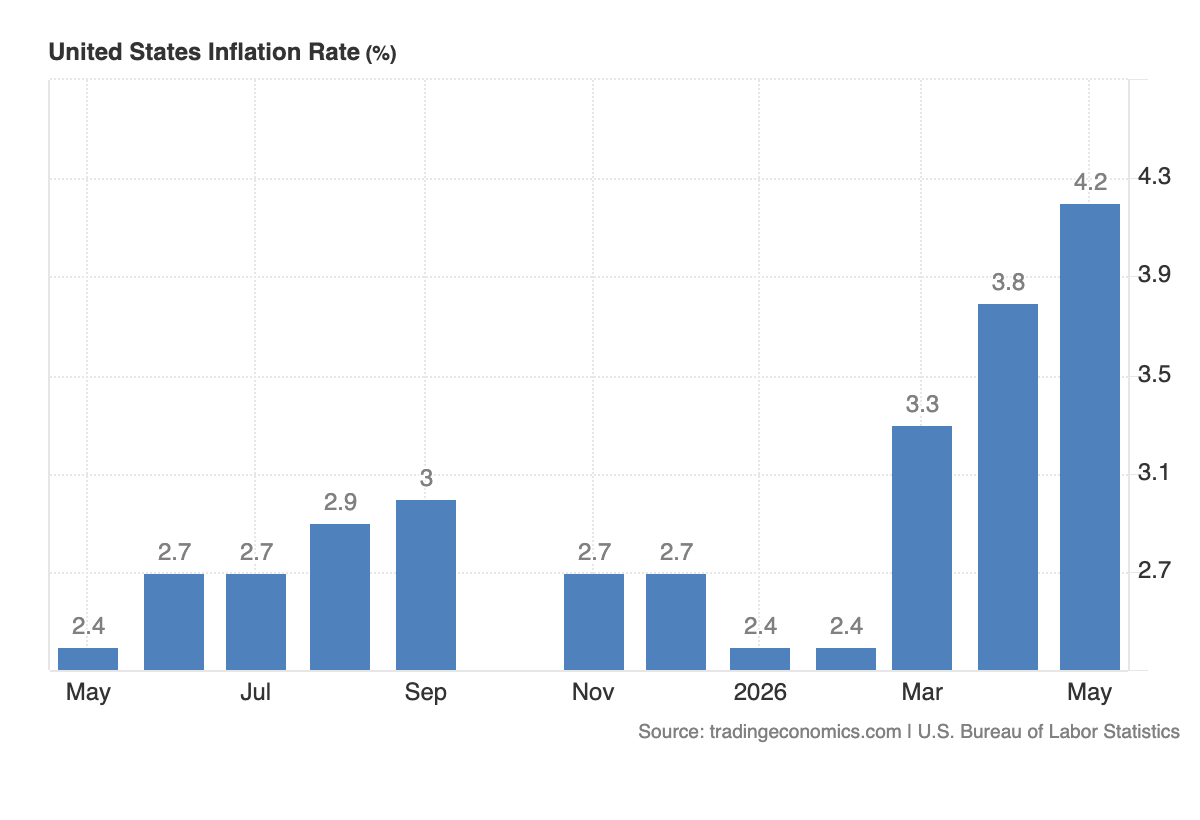

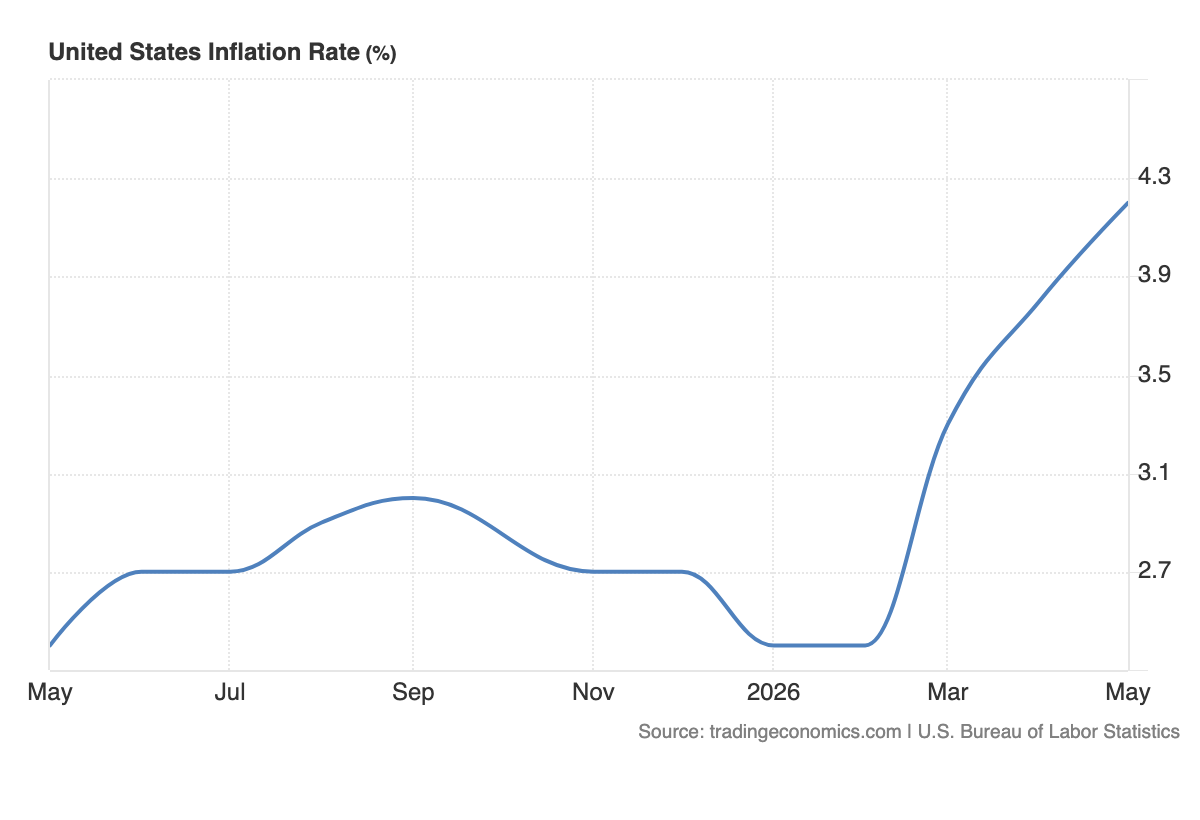

Headline CPI rose to 4.2% in May from 3.8% in April, marking the third straight monthly acceleration and the highest annual inflation rate since April 2023. On the surface, the monthly number was not a major surprise, with CPI rising 0.5% in line with expectations and slightly below April’s 0.6% increase. But the composition of the report is the problem.

This was an energy-led inflation shock.

Energy prices rose 23.5% from a year earlier, while gasoline surged 40.5% and fuel oil climbed 58.9%. Energy also accounted for more than 60% of the monthly increase in headline CPI. That tells markets one thing clearly: inflation is not being driven by a clean demand boom. It is being driven by the Middle East conflict and the disruption to energy supply.

That distinction matters, but it does not make the Fed’s job easier.

The Iran war has kept pressure on oil markets by threatening supply flows through the Strait of Hormuz and raising the risk premium across global energy. When oil prices rise this sharply, the impact does not stay limited to petrol stations. It moves into transport costs, airline fares, food distribution, production costs and import prices. That is how an energy shock becomes a broader inflation problem.

The core CPI details were softer, but not soft enough to change the policy story. Core inflation rose 2.9% year on year, up from 2.8% in April, although the monthly core reading cooled to 0.2% from 0.4%. That gives the market a small relief point, because underlying inflation is not accelerating as aggressively as headline inflation. But the Fed cannot ignore headline inflation when energy is hitting consumers directly and food and shelter are also rising.

Shelter inflation accelerated to 3.4%, while food inflation rose to 3.1% from 2.3%. That makes the report politically and economically sensitive. Households are not only paying more at the pump. They are also seeing pressure in essentials, which affects confidence, spending behaviour and wage demands.

This is where Trump’s latest remarks matter.

Trump tried to present the inflation spike as manageable, arguing that energy prices should come down once the Iran war ends. He also framed the numbers positively, suggesting the market should look through the temporary war effect. The problem is that bond markets and the Fed do not operate on political reassurance. They need evidence that inflation is actually cooling.

Right now, the evidence is mixed at best.

Yes, core inflation cooled month on month. But headline inflation is accelerating, energy is driving most of the increase and the conflict has not been fully resolved. Until oil prices fall meaningfully and stay lower, markets will treat the inflation risk as active.

That is why this CPI print matters for yields.

When inflation rises, bond investors demand more compensation to hold longer-term debt. That pushes Treasury yields higher. Higher yields then tighten financial conditions, support the dollar and pressure assets that do not pay interest, especially gold.

This is the same macro chain markets have been trading for weeks.

The war keeps oil elevated. Higher oil lifts inflation. Higher inflation pushes yields higher. Higher yields keep the Fed hawkish. A hawkish Fed supports the dollar. Gold struggles because the opportunity cost of holding it rises.

That is why the CPI report is not just an inflation story. It is a Fed story.

The Federal Reserve is now facing a difficult mix. Inflation is moving higher, but part of the pressure is coming from an external supply shock. The Fed cannot produce more oil or reopen Hormuz. But it can respond if higher energy prices start feeding into inflation expectations, wages or broader price-setting behaviour.

That is the reaction function.

If the Fed believes the shock is temporary and contained, it can hold rates steady and wait. If the shock becomes persistent, it has to stay restrictive for longer. If inflation expectations rise too far, the discussion can shift from holding rates to hiking again.

That is why markets are not pricing rate cuts anymore.

A 4.2% inflation rate, combined with resilient labour data, gives the Fed very little room to ease. Strong jobs mean the economy is still holding up. Hot inflation means the Fed cannot justify cuts. Together, they keep the higher-for-longer narrative intact and leave the door open for a rate hike before year-end.

The dollar benefits from this setup.

Higher US yields make dollar assets more attractive, while geopolitical uncertainty adds safe-haven demand. Even if Trump argues that inflation will fall once the war ends, the dollar is still supported as long as markets believe the Fed must stay restrictive.

Gold remains under pressure for the same reason.

Inflation caused by war can create safe-haven demand, but this particular shock is also pushing yields higher. That is bad for bullion. Gold can bounce when fear rises, but it struggles when inflation and Fed pricing dominate.

Risk assets face a more complicated picture.

The softer monthly core CPI reading gives equities a small relief point, especially for growth stocks. But headline inflation above 4%, energy prices surging and Fed cuts disappearing are not clean risk-on conditions. Higher fuel costs hit consumers. Higher input costs pressure margins. Higher yields compress valuations.

So the current picture is clear.

Trump is trying to frame this inflation spike as temporary and war-related.

Markets are treating it as a policy problem.

The difference matters.

If the Iran conflict cools and oil prices fall quickly, inflation pressure can ease and the Fed may avoid becoming more hawkish. But if energy prices remain elevated, the May CPI print becomes part of a larger inflation trend rather than a one-off shock.

That is the key risk now.

Inflation is not just above target. It is accelerating again.

And until oil cools, the Fed stays trapped.