The inflation shock may have peaked.

But it has not disappeared.

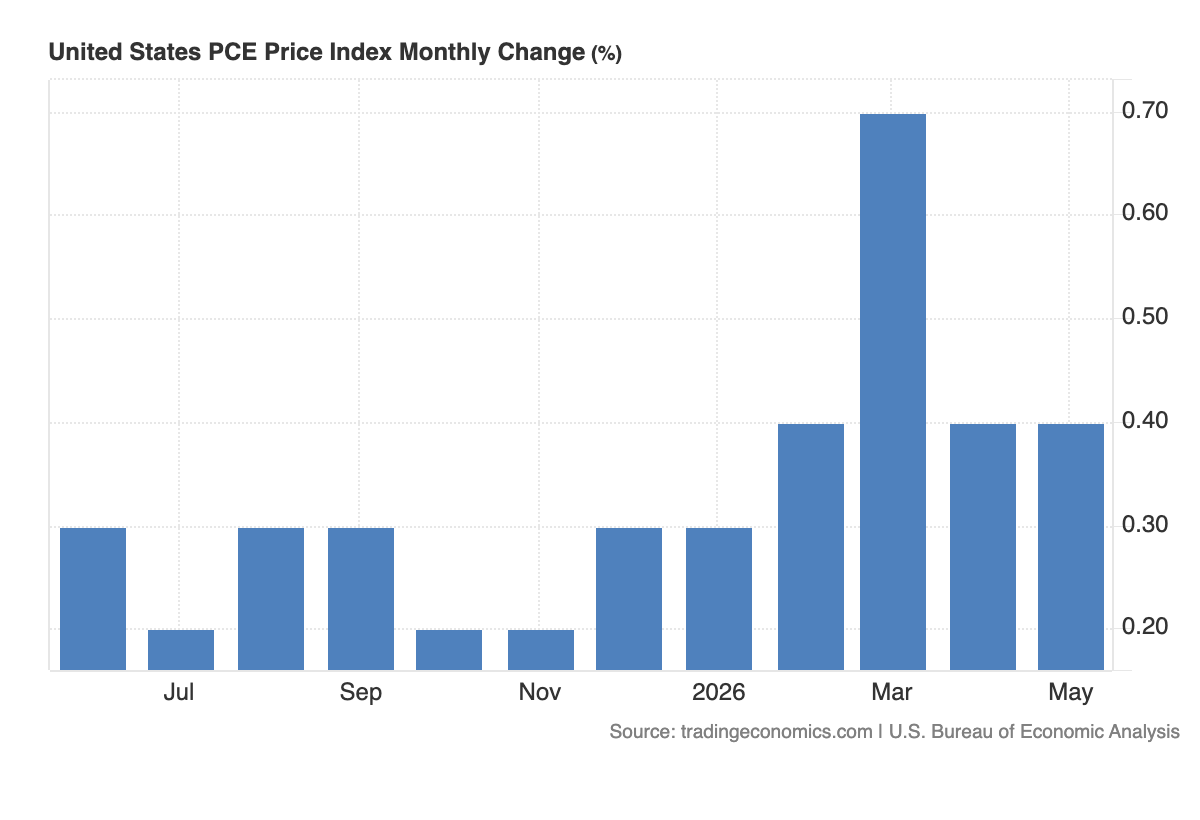

The latest Personal Consumption Expenditures (PCE) report, the Federal Reserve's preferred inflation measure, confirmed that price pressures remain well above the central bank's target despite improving conditions in energy markets.

Headline PCE rose 0.4% in May, slightly below expectations, while annual inflation accelerated to 4.1%, marking its highest level since April 2023. Core PCE, which strips out volatile food and energy prices, also remained elevated at 3.4%, its highest reading since October last year.

Taken together, the data reinforces one message.

Inflation is cooling much more slowly than the market had hoped.

That explains why expectations for another Federal Reserve rate hike remain firmly on the table.

At the Fed's June meeting, policymakers left interest rates unchanged but delivered a distinctly hawkish message. Officials sharply raised their inflation forecasts, projecting headline PCE inflation at 3.6% this year and core PCE at 3.3%, both well above the Fed's 2% objective.

The latest data validates that outlook.

Although monthly inflation met expectations rather than exceeding them, the broader trend remains one of persistent price pressures rather than rapid disinflation.

The story becomes more interesting when viewed through the lens of recent developments in the Middle East.

For much of the past several months, inflation was being driven by a historic energy supply shock.

The conflict involving Iran and the disruption of shipping through the Strait of Hormuz sent oil prices above $110 per barrel, feeding directly into transportation costs, manufacturing expenses and household energy bills. That surge pushed both CPI and PPI sharply higher and forced central banks around the world to adopt a more cautious stance.

Now the backdrop is changing.

Following the US-Iran peace agreement, shipping through Hormuz has steadily recovered, Iranian oil exports have resumed under a temporary US waiver, and Gulf producers have restored a significant share of lost production.

Oil has fallen toward $72 per barrel, close to levels seen before the conflict escalated.

Yet inflation remains elevated.

That highlights an important reality about monetary policy.

Oil prices influence inflation immediately.

But lower oil prices take much longer to work their way through the economy.

Businesses typically do not cut prices overnight simply because fuel becomes cheaper. Existing contracts, wage growth and service-sector costs tend to keep inflation elevated even after commodity prices begin falling.

That lag is exactly what the Federal Reserve is watching.

Officials want evidence that easing energy costs are translating into broader disinflation across the economy, particularly in services, where inflation actually accelerated in the latest report.

The labor market also continues to support the Fed's cautious approach.

Recent payroll reports and job openings data have consistently pointed to a resilient economy rather than one slipping into recession. Strong employment supports household spending, allowing businesses greater pricing power and making inflation more difficult to bring back to target.

That combination explains why several major Wall Street banks, including Deutsche Bank and Bank of America, continue to expect another Fed rate hike later this year.

Markets have largely aligned with that view.

Treasury yields remain elevated, reflecting expectations that interest rates will stay higher for longer. The dollar has also remained well supported as investors continue favoring US assets offering relatively attractive returns.

Gold, meanwhile, has struggled.

Even though geopolitical tensions have eased and oil prices have retreated, bullion continues facing pressure from higher real yields and a stronger dollar. As long as investors believe the Fed is not finished fighting inflation, non-yielding assets are likely to remain under pressure.

Looking ahead, the key question is whether this PCE report represents the peak in inflation or merely another step in a prolonged battle against rising prices.

The normalization of global energy markets should gradually reduce inflation over the coming months.

But the Fed has made one point clear.

It will respond to the data, not the hope.

Until inflation begins moving decisively back toward 2%, policymakers are unlikely to soften their stance.

For markets, that means the conversation has shifted.

The focus is no longer on whether inflation is rising.

It is on how long inflation will remain high enough to keep interest rates elevated.

And after today's report, the answer appears to be longer than many investors were expecting.