The UK housing market just showed the first real sign of pressure from the energy shock.

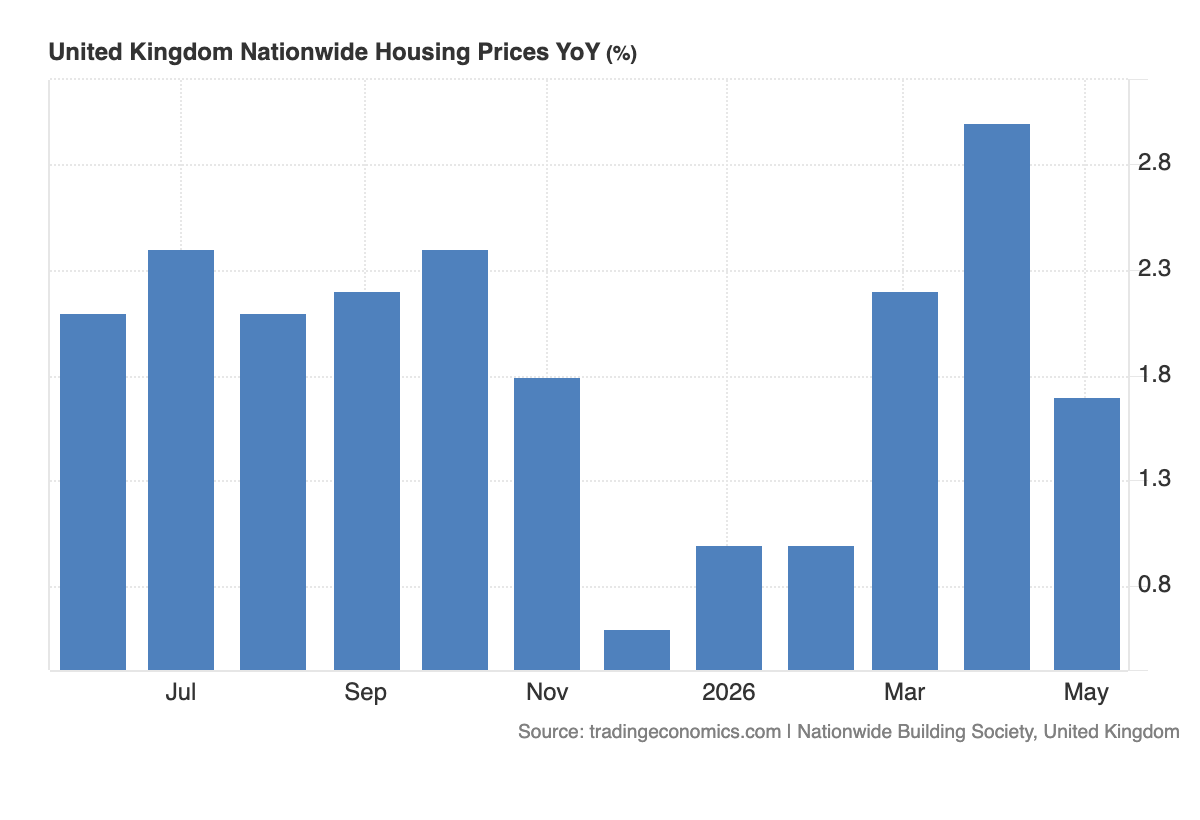

Nationwide reported that house prices fell 0.6% in May, the first monthly decline in five months, while annual growth slowed to 1.7% from 3.0% in April. Reuters reported that the fall was steeper than economists expected, with Nationwide linking the slowdown to uncertainty from the Iran war, higher energy prices and rising market interest rates.

This is not just a property story.

It is the housing market reacting to the same macro chain that has been hitting bonds, currencies and commodities.

The starting point is energy.

The Middle East conflict has pushed up oil and gas prices, feeding inflation risk across major economies. The Bank of England has already warned that the conflict makes the outlook for global energy prices highly uncertain. It also noted that monetary policy cannot directly control energy prices, but it can respond if those price shocks feed into broader inflation expectations.

That is exactly why UK mortgage rates matter.

Higher energy prices raise inflation risk. Higher inflation risk pushes market interest rates higher. Higher market rates feed into swap rates, and swap rates influence mortgage pricing. Once mortgage rates rise, affordability weakens and buyers become more cautious.

That is the transmission.

Oil rises.

Inflation risk rises.

Market rates rise.

Mortgage rates rise.

Housing demand softens.

That is what May’s Nationwide data is showing.

The UK entered this shock with some support. The economy grew strongly in the first quarter, with reports pointing to 0.6% growth, helped by services activity. Inflation had also been easing before the energy shock became the dominant risk.

That is why this does not yet look like a housing crash.

Household balance sheets are not in the same weak position seen during earlier stress periods. Nationwide’s Robert Gardner argued that household finances remain relatively healthy, supported by low debt levels, savings buffers and improving affordability. That means the housing market can absorb some pressure if energy prices stabilize and geopolitical tensions ease.

But the warning is still real.

Mortgage rates are already moving in the wrong direction for buyers. Reuters reported that average two-year and five-year fixed mortgage rates have risen to around 5.13% and 5.15%, roughly half a percentage point higher than a year earlier. The Guardian reported even higher average two-year fixed pricing, showing that borrowing costs remain a major drag on demand.

That creates a confidence problem.

Even buyers who can afford to move may delay decisions when mortgage rates are volatile, energy bills are rising and geopolitical risk is feeding uncertainty. Housing is highly sensitive to confidence because the transaction is large, debt-funded and long-term. When households are unsure about income, rates or inflation, they wait.

That is why the monthly drop matters more than the annual number.

Annual growth of 1.7% still looks positive. But the monthly decline shows the momentum has turned weaker. The housing market is moving from recovery mode into caution mode.

For the Bank of England, this is a difficult setup.

A weaker housing market normally argues for caution. If higher mortgage rates start weighing on demand, consumption and construction activity, the BoE has less reason to tighten aggressively.

But the inflation side is not clean.

Energy-driven inflation can keep headline prices elevated even as housing demand softens. That is the uncomfortable policy trade-off. The BoE may not want to tighten into a slowing housing market, but it also cannot ignore inflation if energy costs keep feeding into expectations and wages.

So policy becomes constrained.

Not clearly hawkish.

Not comfortably dovish.

Just stuck.

That matters for the pound and UK yields.

If the market believes inflation risk will keep the BoE cautious, gilt yields can stay supported. But if housing and consumer demand weaken more sharply, markets may start pricing lower growth and eventual policy relief. Sterling then becomes caught between two forces: rate support from inflation risk and growth pressure from weaker domestic demand.

For equities, the signal is also mixed.

Lower house prices and higher mortgage rates pressure homebuilders, banks and consumer-facing sectors. But if falling oil prices or a peace deal reduce inflation pressure, rate expectations can ease, helping risk assets recover.

That is why the next move depends heavily on energy.

If Middle East tensions ease and oil stabilizes, the UK housing slowdown could prove temporary. Mortgage rates may soften, confidence may improve and buyers could return.

If the conflict drags on and energy prices stay elevated, the pressure becomes more persistent. Mortgage rates remain high, affordability worsens and demand weakens further.

The current picture is clear.

UK house prices are not falling because the domestic economy collapsed.

They are falling because the external energy shock has pushed through the rates channel.

Oil has lifted inflation risk.

Inflation risk has lifted market rates.

Higher market rates have lifted mortgage costs.

And higher mortgage costs are now hitting housing demand.

That is the real story.