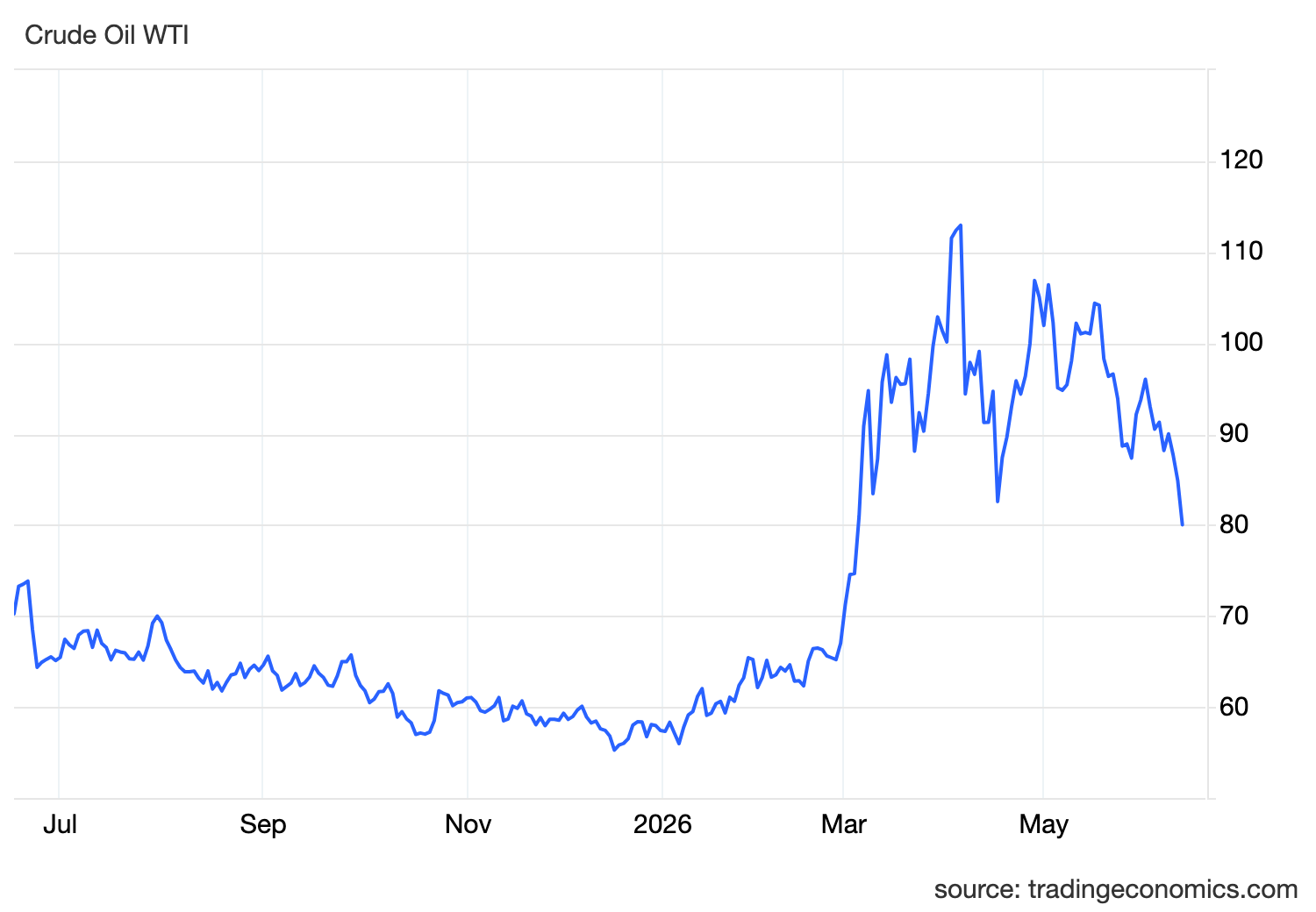

Oil has finally broken lower because the market is pricing the end of the Hormuz shock.

Crude fell more than 5% toward 80, touching a two-month low after the US and Iran reached a peace agreement designed to end the conflict and reopen the Strait of Hormuz by the end of the week. President Donald Trump said oil shipments from the Persian Gulf could soon resume, including the lifting of the US blockade on Iranian ports. Iran also confirmed that a deal had been reached, with the final text expected after a signing ceremony in Switzerland.

This is a major shift.

For months, oil was trading with a heavy war premium because the Strait of Hormuz was effectively closed. That mattered because Hormuz carries roughly one-fifth of global oil shipments. When a chokepoint that important becomes restricted, markets do not just price fewer barrels. They price uncertainty around shipping, insurance, inventories, refinery planning and global energy security.

Now that risk premium is coming out.

The proposed agreement does more than pause hostilities. It reportedly includes a reopening of Hormuz, an end to the blockade on Iranian ports, provisions tied to dismantling Iran’s nuclear program and economic incentives if Tehran meets its commitments. That gives the market a framework for supply normalization rather than just another temporary ceasefire.

That is why the oil move is so sharp.

The market is no longer pricing only disruption. It is now pricing the possibility that energy flows from the Persian Gulf can restart, producers can bring halted supply back online and Asian importers can regain access to one of their most important supply routes.

The macro impact is bigger than crude.

For weeks, the oil shock was the main reason inflation expectations kept rising. Higher oil pushed up fuel costs, transport costs, production costs and import prices. That pressure fed into CPI, PPI and PCE, forcing markets to price out rate cuts and consider the risk of further central-bank tightening.

Now the chain is starting to reverse.

Lower oil eases inflation pressure. Lower inflation pressure reduces the need for bond investors to demand higher yields. Lower yields reduce the pressure on central banks to stay aggressively restrictive. That is why this oil drop matters across every major asset class.

For the Federal Reserve, this is the first genuinely helpful development in weeks.

The Fed has been trapped between strong labour data and rising inflation. Strong jobs gave policymakers room to stay tight, while the oil shock made inflation harder to ignore. If crude keeps falling and Hormuz reopens as planned, the inflation outlook becomes less threatening. That does not mean the Fed immediately cuts rates, but it weakens the case for another hike before year-end.

That is the policy shift markets will now start testing.

Before this deal, the market was focused on whether the Fed might need to tighten again because oil-driven inflation was feeding through the economy. After this deal, the question becomes whether lower energy prices can cool inflation quickly enough to reduce hike risk.

For yields, the direction should be lower if the oil decline holds. Treasury yields rose during the conflict because investors demanded compensation for persistent inflation risk. If oil falls from the shock zone and stays lower, that inflation premium can fade. That would ease financial conditions and support rate-sensitive assets.

For the dollar, the setup becomes less one-sided.

The dollar had been supported by two forces: higher US yields and safe-haven demand from geopolitical uncertainty. A credible US-Iran deal weakens both. If oil falls, inflation pressure cools and Fed hike bets decline. If the conflict ends, defensive dollar demand also fades. That does not automatically mean a dollar collapse, especially if US data stays strong, but it does remove one of the strongest support pillars.

Gold becomes more complicated.

A peace deal reduces safe-haven demand, which is normally negative for gold. But lower oil can also bring down yields, which is positive for gold because bullion does not pay interest. The key question for gold is which force dominates: less fear or lower yields. If yields fall meaningfully, gold can stabilize even as geopolitical fear fades. If the dollar stays firm and investors rotate into risk assets, gold may still struggle.

Risk sentiment should improve.

Lower oil reduces pressure on consumers, corporate margins and inflation expectations. It also lowers the probability that central banks need to tighten further. That is supportive for equities, especially growth and technology stocks, because lower yields make future earnings more valuable.

Asia is one of the biggest winners from this shift.

China, India, Japan and South Korea are heavily exposed to energy imports. A reopening of Hormuz would ease pressure on import bills, inflation, current-account balances and corporate costs. For Japan especially, lower oil helps reduce imported inflation pressure and may give the Bank of Japan more room to move gradually rather than being forced into a faster tightening path.

The deal still has execution risk.

Markets are pricing the announcement, but the actual reopening of Hormuz must happen. The blockade must be lifted, tankers must move safely, insurance conditions must normalize and Iranian commitments must be verified. If the signing is delayed or either side disputes the terms, oil can rebound quickly.

But the direction of the macro story has changed.

Until now, the Middle East conflict was pushing markets into a tighter-policy narrative. Oil was rising, inflation was accelerating, yields were supported, the dollar had a floor and gold was under pressure from real-rate risk.

Now the market is starting to price relief.

Oil is falling because supply normalization is back on the table. Inflation pressure can ease if the decline holds. Yields can cool if inflation expectations reset. Central banks can become less hawkish if the energy shock fades.

The key takeaway is simple.

This is not just an oil selloff.

It is a potential break in the inflation shock that has been driving global markets for months.