Oil is no longer trading on what could go wrong.

It is increasingly trading on what could go right.

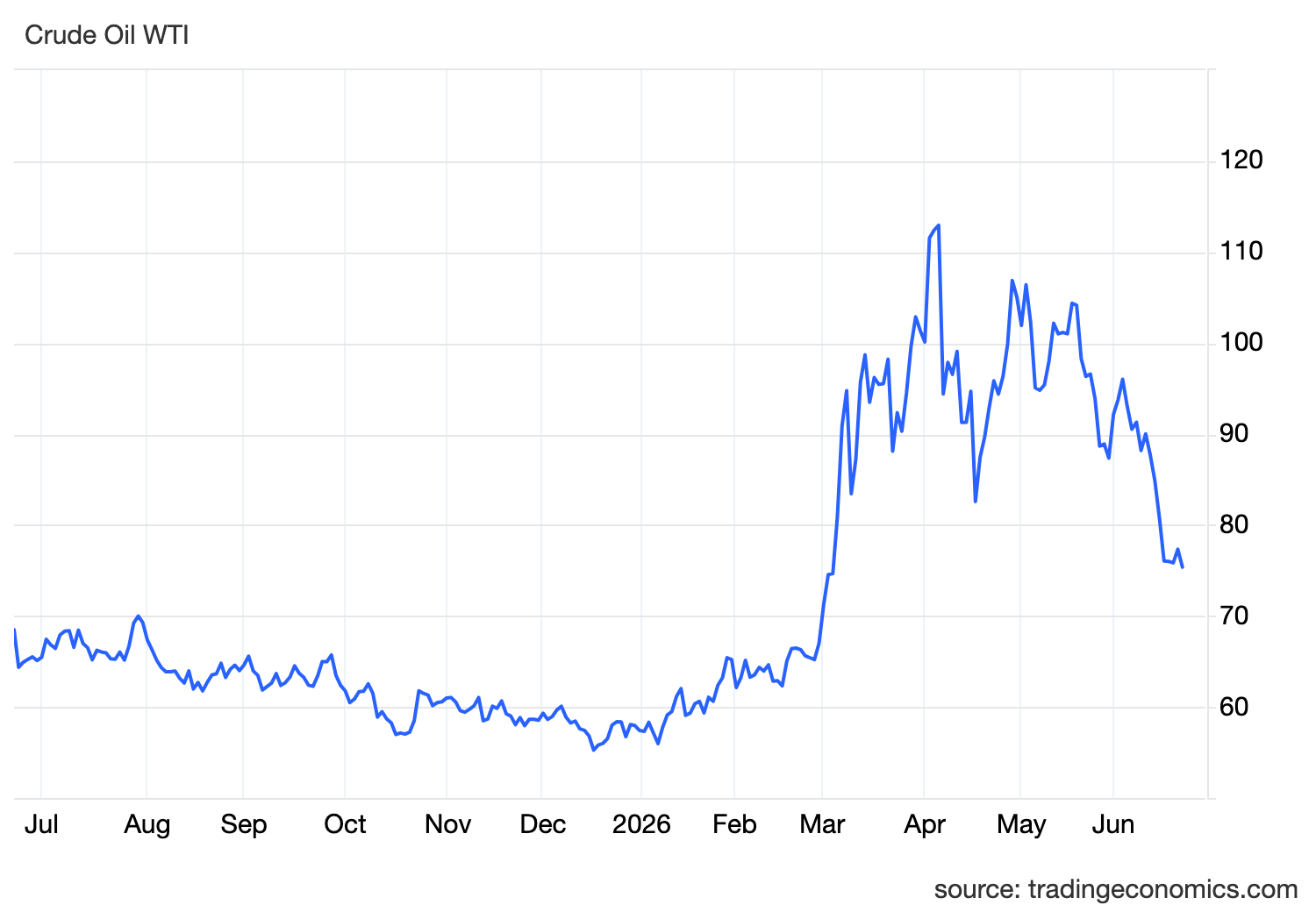

WTI crude slipped below $76 per barrel as investors looked past another round of aggressive rhetoric from Washington and focused instead on tangible progress in negotiations between the US and Iran. According to mediators from Qatar and Pakistan, both sides have agreed to a roadmap aimed at securing a final peace agreement within the next 60 days.

That development matters because the market is beginning to transition from a supply shock narrative to a supply recovery narrative.

For months, the closure of the Strait of Hormuz was the dominant macro story. The disruption affected one of the world's most important energy corridors, creating a historic supply shock that pushed oil sharply higher and became a major driver of inflation across advanced economies.

The impact extended far beyond energy markets.

Higher crude prices fed directly into transportation costs, manufacturing inputs, logistics expenses and household energy bills. Those pressures eventually appeared in inflation data around the world.

In the United States, CPI accelerated to 4.2%, its highest level since 2023, while producer prices recorded their fastest increase since 2022. Similar pressures emerged across Europe and Asia, forcing central banks to reassess their policy outlooks.

The Federal Reserve's latest meeting reflected that reality.

While policymakers left rates unchanged, they sharply upgraded inflation forecasts and revealed that roughly half of FOMC members still expect at least one rate hike ahead. The ECB recently delivered its first rate increase since 2023, while the Bank of Japan raised rates to 1.0%, the highest level since 1995.

In many ways, the oil shock became the defining macro event of the year.

Now markets are trying to determine how quickly that process can unwind.

The latest negotiations suggest the path toward normalization may be accelerating.

Millions of barrels of crude continued flowing through Hormuz over the weekend, and Gulf producers are already preparing to increase output. If a final agreement is reached and shipping conditions fully normalize, the market could face a significant increase in available supply over the coming months.

That prospect helps explain why traders largely ignored the latest threats from President Trump.

Earlier in the session, oil initially moved higher after Trump warned of possible military action if Hezbollah attacks continue and cautioned Iran against attempting to close Hormuz again. Iranian media subsequently reported a suspension of talks.

Under different circumstances, those headlines could have triggered a much larger rally.

Instead, prices faded.

The market appears increasingly convinced that neither side wants to derail negotiations entirely. Investors are placing greater weight on the diplomatic process than on periodic political escalation.

This shift is important because lower oil prices could begin influencing broader macro expectations.

For much of the first half of the year, rising oil translated into higher inflation expectations, higher bond yields and more hawkish central bank pricing.

Now the opposite risk is emerging.

If oil continues falling toward pre-conflict levels, inflation pressures could begin easing more materially during the second half of the year. That would reduce pressure on central banks to tighten further and potentially improve financial conditions across global markets.

Treasury yields have already started stabilizing after their sharp rise following recent inflation reports. Equity markets have responded positively as investors anticipate lower energy costs and reduced inflation risks.

The dollar may also face a more complicated environment.

Recent dollar strength was supported by expectations that persistent inflation would keep US rates elevated. If oil continues falling and inflation gradually moderates, some of that support could begin fading, particularly if other major economies maintain restrictive policy settings.

For global growth, the implications are potentially significant.

The energy shock acted as a tax on consumers and businesses. Lower fuel costs would ease pressure on household spending, improve corporate margins and support economic activity at a time when many economies are already showing signs of slowing momentum.

That is why oil is becoming one of the most important indicators to watch.

The market is no longer asking whether a supply shock occurred.

That question has already been answered.

The new question is whether supply normalization can arrive quickly enough to reverse the inflation pressures that reshaped monetary policy over the past several months.

For now, investors appear increasingly confident that it can.

That confidence is showing up in lower oil prices.

And if it proves justified, the effects will extend well beyond the energy market.