Oil is falling because the market is finally seeing a possible path out of the supply shock.

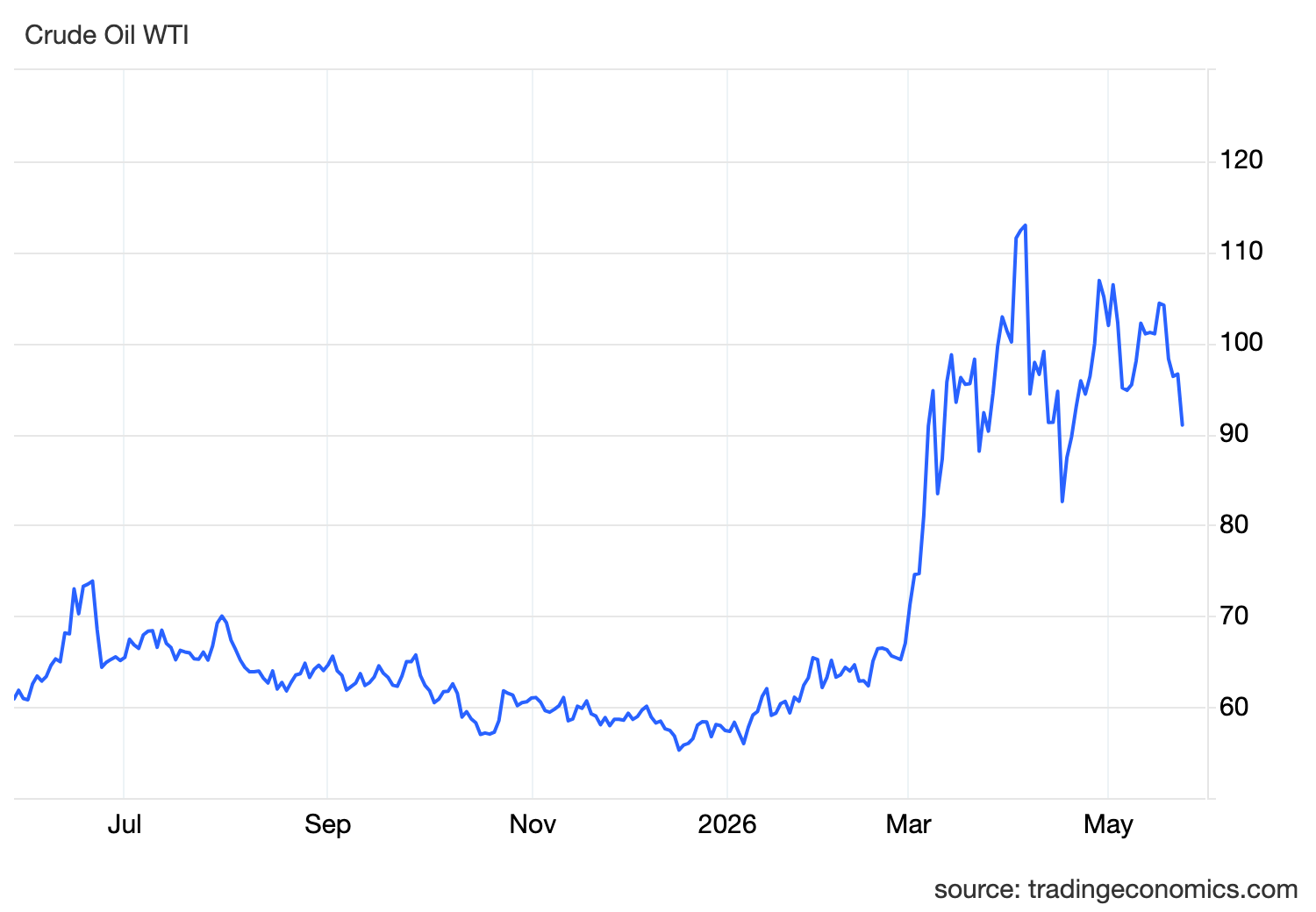

WTI dropped toward 91, extending last week’s decline, after reports suggested the US and Iran were moving closer to a deal. The proposed agreement could reopen the Strait of Hormuz, end hostilities, release some frozen Iranian assets and create a framework for further nuclear talks.

That is the immediate trigger.

But the bigger market move is about risk premium.

For weeks, oil was trading with a heavy war premium because Hormuz was effectively shut, regional supply was disrupted and producers were forced to halt millions of barrels per day in output. Now traders are starting to price the opposite scenario: not full normalization yet, but a credible route toward reopening.

That is why crude is dropping sharply.

Reuters reported that oil prices fell to two-week lows as optimism improved around a possible US-Iran agreement, with WTI trading near 90.85 and Brent below 98. The same report still noted that disagreements remain, especially around the blockade and the timing of any reopening.

This distinction matters.

Oil is not falling because the problem is solved.

Oil is falling because the probability of resolution has increased.

President Trump has also made it clear that Washington will not rush the process and that the US blockade remains in place until a verified agreement is signed. That keeps some risk premium in the market, because traders still need proof, not promises.

The Strait of Hormuz is the centre of the whole setup.

The IEA describes Hormuz as one of the world’s most critical oil transit chokepoints, with around 20 million barrels per day of crude and oil products moving through it in 2025. It also estimates that about 25% of global seaborne oil trade passes through the strait, with limited alternatives if flows are disrupted.

That is why a reopening would be a major macro event.

It would not just lower oil.

It would lower the inflation shock.

Over the past few weeks, the market has been trading a simple chain.

Hormuz disruption pushed oil higher.

Higher oil lifted inflation expectations.

Hotter inflation pushed yields higher.

Higher yields forced markets to price out Fed cuts.

The dollar strengthened.

Gold struggled.

Risk assets faced tighter financial conditions.

Now that chain is starting to reverse.

If Hormuz reopens, crude supply confidence improves. If crude prices fall, energy-driven inflation pressure eases. If inflation pressure eases, Treasury yields can stabilize or decline. If yields cool, the Fed has less pressure to sound hawkish. That is why this oil move matters across every asset class.

This is especially important after last week’s inflation data.

US CPI and PPI had already shown that the energy shock was feeding into the broader price system. That pushed markets toward a higher-for-longer Fed view and even revived discussion around a possible hike later in the year. Lower oil does not erase those prints, but it can reduce the risk that the next inflation wave becomes worse.

That matters for the Federal Reserve.

The Fed cannot cut simply because oil has one weak session. But if oil keeps falling and Hormuz progress becomes real, the inflation outlook improves. That would reduce pressure on policymakers to keep leaning hawkish and could take some heat out of rate-hike expectations.

For yields, this is relief.

Bond markets had been selling off because investors were demanding more compensation for inflation risk. Lower crude reduces that pressure. If energy prices continue falling, the 10-year yield can come off recent highs because the inflation premium starts to fade.

For the dollar, the setup becomes less supportive.

The dollar had benefited from higher US yields and geopolitical safe-haven demand. A credible US-Iran deal weakens both drivers. It reduces fear, lowers oil inflation risk and softens the case for a more restrictive Fed.

For gold, the reaction is more nuanced.

Lower geopolitical risk can reduce safe-haven demand. But lower oil also reduces inflation pressure and can pull yields down, which is supportive for gold. So gold’s reaction depends on which force dominates: less fear or lower yields.

For risk assets, the oil drop is constructive.

Lower energy prices reduce margin pressure, ease household cost pressures and reduce the probability of aggressive central-bank tightening. That is the kind of relief equities want, especially after weeks of oil-driven inflation stress.

Asia is also central here.

A full Hormuz reopening would be especially important for major Asian economies because much of the oil and LNG passing through the strait is destined for Asia. The IEA notes that around 80% of oil and oil products transiting Hormuz in 2025 went to Asian markets, while Hormuz also carried a major share of global LNG trade.

That means lower oil would help China, India, Japan and South Korea through reduced import costs, lower inflation pressure and improved external balances.

But the market still needs confirmation.

Trump has said he will not rush into a deal. The blockade remains in place. Nuclear negotiations are still unresolved. And even if a deal is signed, shipping confidence does not return instantly. Insurance costs, vessel routing, port backlogs and producer output all take time to normalize.

So the correct read is this.

Oil is dropping because peace odds improved.

But the supply shock is not fully resolved.

If a formal deal is signed and Hormuz reopens, crude can fall further and the inflation pressure can cool meaningfully.

If talks stall again, oil can snap back quickly because the physical supply risk has not disappeared.

For now, the market is moving from panic pricing to conditional relief.

That is the key.

Lower oil is giving markets breathing room.

But until Hormuz actually reopens, it is relief, not resolution.