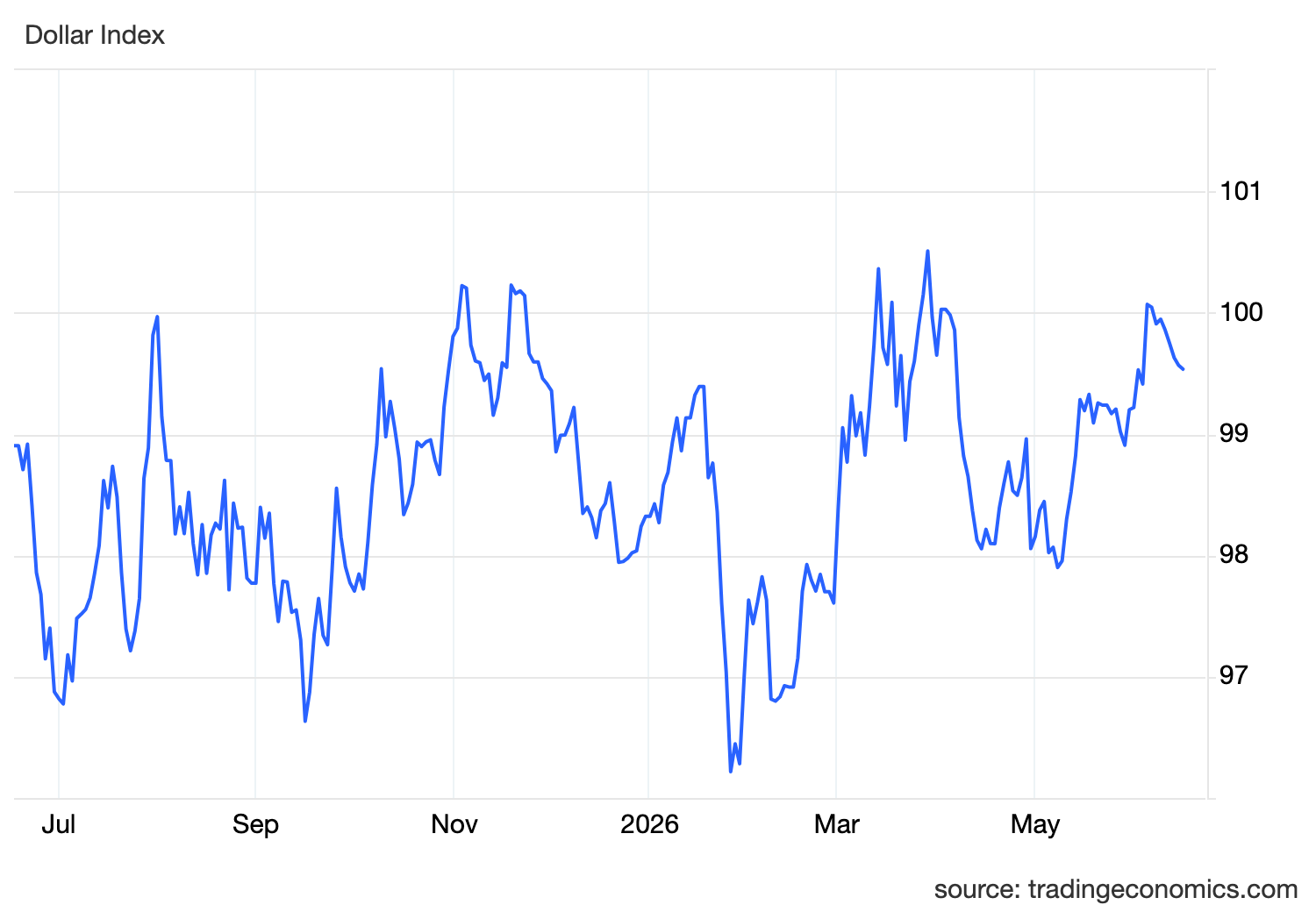

The dollar is entering a pivotal week caught between two competing forces.

On one side, the Federal Reserve is expected to leave rates unchanged at its first meeting under new Chair Kevin Warsh. On the other, the global inflation shock that dominated markets for months is beginning to ease as the US-Iran peace agreement moves toward formal signing and the reopening of the Strait of Hormuz.

That shift matters far beyond oil markets.

The closure of Hormuz was the defining macro catalyst of the past several months. The disruption removed millions of barrels per day from global energy markets, sending oil sharply higher and feeding directly into inflation data across major economies.

The impact became increasingly visible in the United States.

Recent CPI and PPI reports showed inflation accelerating for three consecutive months, driven largely by energy costs. Headline CPI reached 4.2%, its highest level since 2023, while producer prices recorded their strongest increase since 2022. Combined with resilient labor market data, including stronger-than-expected payrolls and job openings, investors were forced to abandon expectations for rate cuts and instead begin pricing the possibility of another Fed hike before year-end.

That repricing helped push Treasury yields higher and supported the dollar throughout much of the conflict.

Now the market is asking whether that process has peaked.

The proposed US-Iran agreement is expected to reopen Hormuz and restore energy flows through one of the world's most important shipping corridors. Oil prices have already fallen to two-month lows in anticipation.

If those declines persist, the inflation impulse that dominated recent data may begin to fade in the months ahead.

Importantly, however, central banks cannot react to future inflation relief before it appears in the data.

That is why the Fed is still expected to remain cautious.

While lower oil reduces future inflation risks, policymakers must still deal with current inflation running above target and an economy that continues to show surprising resilience. Retail spending, employment and business activity have yet to show the type of deterioration that would justify a more accommodative stance.

As a result, markets expect rates to remain unchanged, but investors will scrutinize Warsh's language for clues about whether the Fed still sees additional tightening as a realistic possibility.

The significance of this meeting extends beyond the United States because global central banks are increasingly moving in different directions.

Earlier this week, the Bank of Japan raised interest rates to 1.0%, its highest level since 1995. The move reflects mounting concern over imported inflation, producer price pressures and years of yen weakness. Japan is now actively normalizing policy after decades of ultra-loose monetary conditions.

Meanwhile, the Reserve Bank of Australia left rates unchanged at 4.35%. Policymakers acknowledged softer labor market conditions and appear comfortable waiting for additional evidence before considering further action.

These diverging policy paths matter for currencies.

The BoJ's tightening cycle has the potential to support the yen by narrowing the enormous rate differential that has favored the dollar for years. At the same time, a Fed that remains restrictive continues to provide support for the greenback.

That tension helps explain why the dollar has remained relatively stable despite the collapse in oil prices.

Treasury yields are also becoming increasingly important.

Much of the dollar's recent strength came from rising yields driven by inflation concerns. If lower oil prices eventually translate into softer inflation readings, yields could begin to moderate, reducing one of the dollar's strongest sources of support.

For now, however, investors remain cautious about assuming that outcome.

The inflation surge caused by the energy shock has already worked its way through global supply chains, transportation costs and consumer prices. Even if oil remains lower, central banks will likely require several months of evidence before shifting their policy outlooks.

That leaves markets in a transition phase.

The immediate inflation shock appears to be fading.

The policy response to that shock remains restrictive.

And investors are trying to determine which force will dominate the second half of the year.

For the dollar, the answer depends largely on whether incoming economic data confirms that inflation is beginning to cool without a significant deterioration in growth.

That is why this week's Fed meeting, retail sales figures and housing data matter so much.

Markets are no longer focused solely on how high inflation has become.

They are increasingly focused on whether the inflation cycle itself has finally turned.