Gold is still under pressure because the market has two reasons to keep the Fed hawkish.

The first is inflation.

The second is labour market resilience.

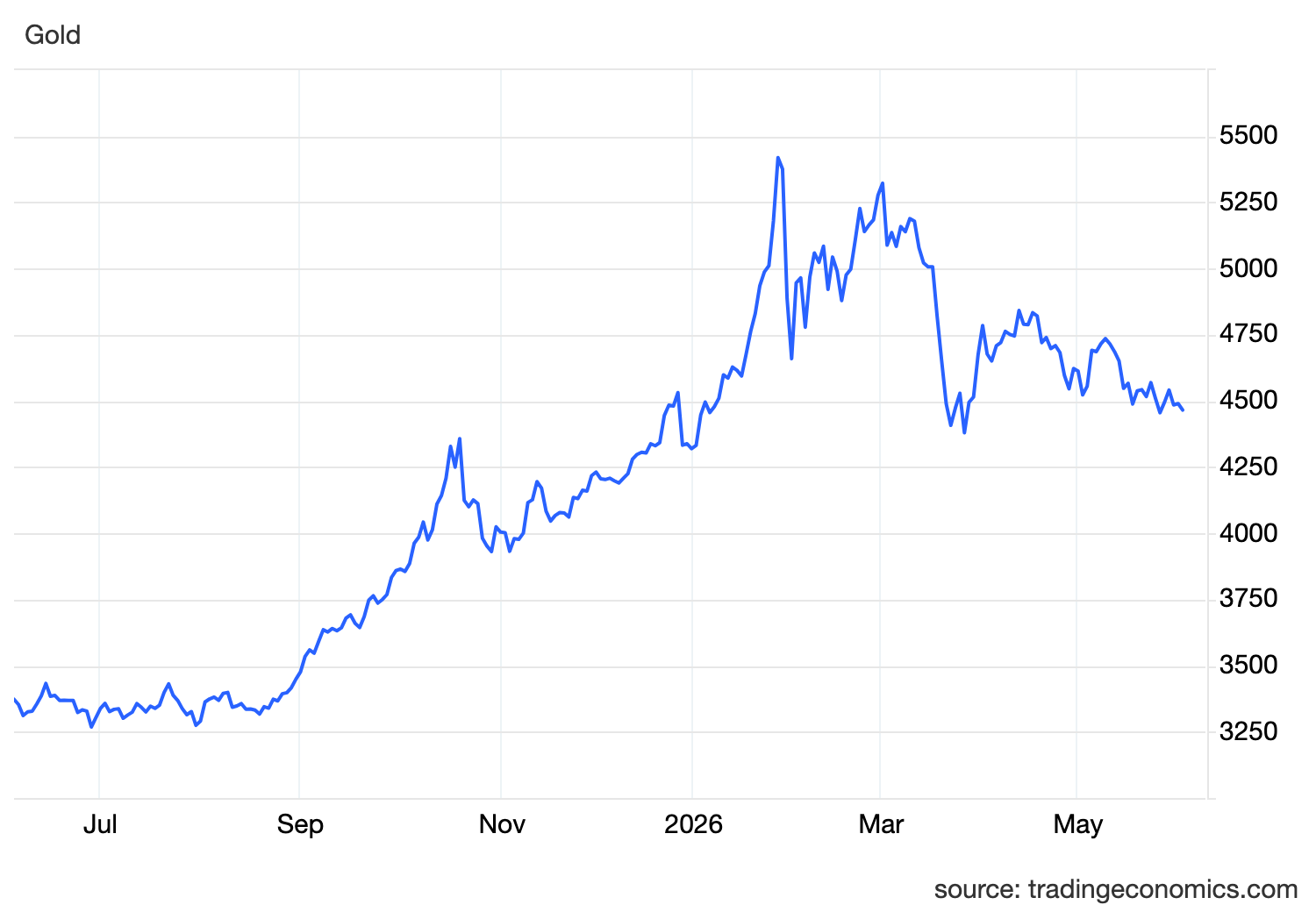

Gold held below 4500 after losses earlier in the week, as stronger-than-expected US labour data pushed investors back toward the higher-for-longer trade. April job openings jumped to 7.6 million, up from 6.9 million in March and above expectations, while layoffs declined. The Labor Department’s JOLTS data showed openings rising to their highest level since May 2024, although hiring and quits both softened, which suggests firms are still cautious even as labour demand remains firm.

That matters for gold because the Fed reaction function is simple.

If inflation is hot but the labour market is weak, the Fed has a dilemma.

If inflation is hot and the labour market is still holding, the Fed has room to stay restrictive.

Right now, the second setup is winning.

The labour market is not booming across every detail, but it is also not breaking. Job openings are rising, layoffs are lower, and the unemployment backdrop has not weakened enough to force the Fed into a growth-support mode. That means Friday’s nonfarm payrolls report now becomes critical.

Markets are not just watching jobs.

They are watching whether jobs give the Fed permission to stay tight.

The inflation side is still being driven by oil.

US-Iran peace negotiations remain uncertain, and that keeps oil prices supported. President Trump says talks remain underway, while reports suggest Iranian officials are reviewing a final text that could be sent back to Washington. That gives markets some hope, but not enough confirmation to remove the energy risk premium.

The Strait of Hormuz remains the key channel.

If negotiations succeed and shipping normalizes, oil can fall, inflation pressure can ease, and yields can cool.

If talks fail and oil rises again, inflation risk stays alive, and the Fed remains boxed in.

That is why gold is not getting a clean safe-haven rally.

The conflict creates uncertainty, which should normally support bullion. But this war has repeatedly hurt gold through the inflation and rates channel. Oil rises, inflation expectations rise, yields rise, Fed cuts get priced out, the dollar strengthens, and gold struggles.

The latest inflation data has already pushed the market in that direction.

April CPI and PPI showed that the energy shock is feeding into consumer and producer prices, while the Fed’s preferred PCE gauge also stayed elevated. Recent reporting showed markets assigning a much higher probability to a year-end hike than to any cut, which captures how far the policy conversation has shifted away from easing.

That is the direct pressure on gold.

Gold does not pay interest. When Treasury yields rise or stay elevated, the opportunity cost of holding gold increases. A firm dollar adds another layer of pressure by making gold more expensive for non-dollar buyers.

This is why gold remains vulnerable below 4500.

It is not because geopolitical risk has disappeared.

It is because the risk is inflationary.

The market is waiting for two confirmations now.

First, NFP.

If payrolls come in strong, it reinforces the idea that the Fed can stay restrictive. That would support yields and the dollar, keeping pressure on gold.

If payrolls weaken meaningfully, gold may find relief, especially if wage growth softens and markets trim Fed hike risk.

Second, Iran talks.

If the final text leads to real progress and Hormuz risk fades, oil can cool. That would ease inflation expectations and give gold a better setup through lower yields.

But if talks break down, oil can rise again. That may create a short-term safe-haven bid for gold, but if the oil move also pushes yields higher, the rally can fade quickly.

So the current setup is clear.

Gold is stuck because labour data is firm and oil risk has not disappeared.

Strong jobs support higher-for-longer policy.

Oil risk keeps inflation alive.

Together, they keep yields supported.

And that keeps gold under pressure.

Until either the labour market weakens or oil-driven inflation cools, gold’s upside remains limited.