Gold is still under pressure because the market is trading inflation, yields and the Fed.

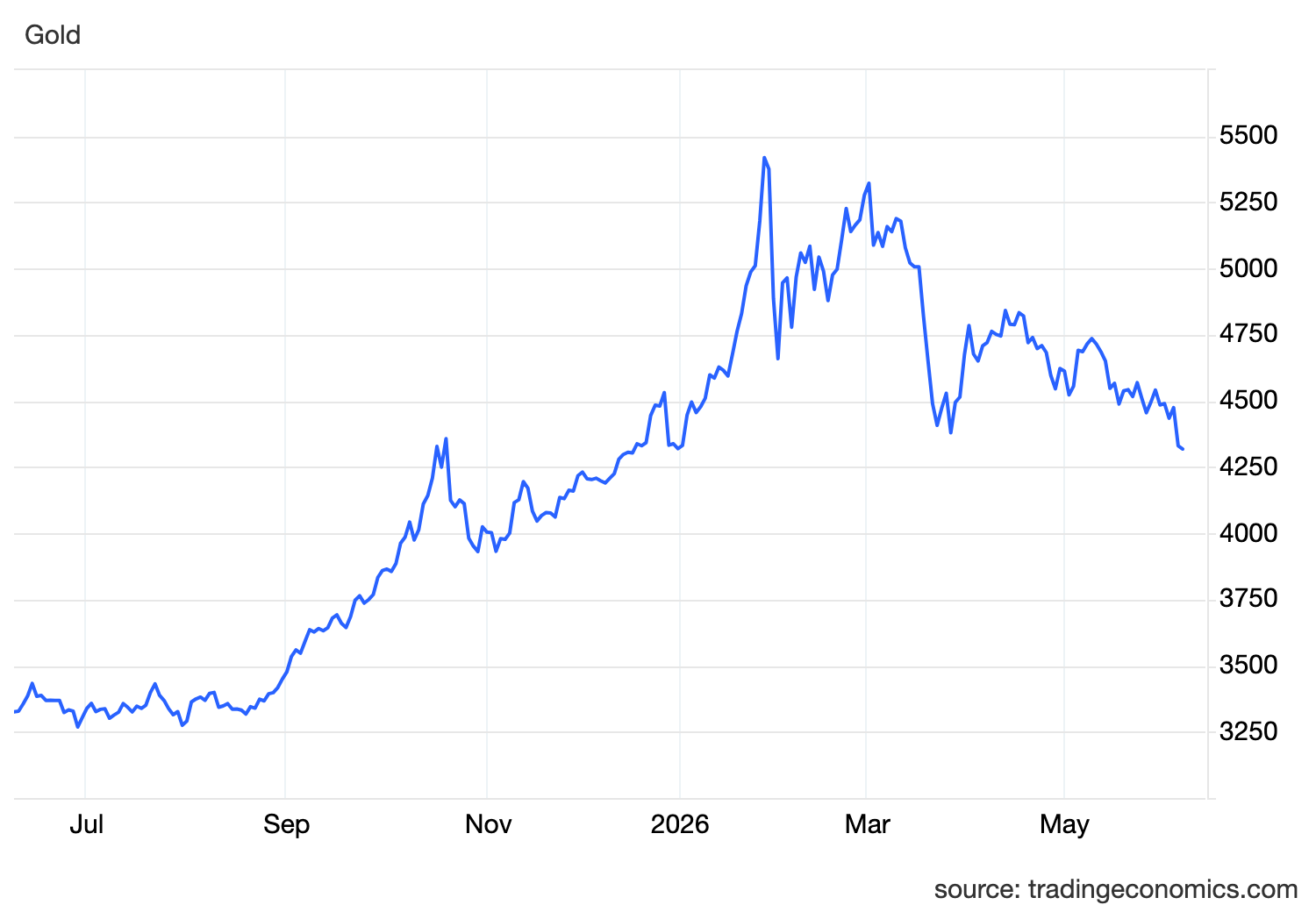

The metal is hovering near 4300 after falling nearly 5% last week, its lowest level in more than two months. The move is important because it confirms the same pattern we have seen throughout this conflict.

Geopolitical risk is not automatically bullish for gold anymore.

The latest escalation came after Iran launched missiles toward Israel in response to military actions in Lebanon. Israel said the projectiles were intercepted and no casualties were reported, which helped prevent a full panic move. But the broader message is still clear.

The Middle East conflict is not resolved.

That matters because the Strait of Hormuz remains near-closed, keeping pressure on global energy supplies from the Persian Gulf. This is the core macro channel. As long as Hormuz remains disrupted, oil prices stay supported. As long as oil stays supported, inflation risk remains alive.

That is why gold is struggling.

Under normal conditions, missile strikes, regional conflict and rising uncertainty would create a clean safe-haven bid for gold. But this war is creating a different market reaction because it is directly feeding inflation.

Oil rises.

Inflation expectations rise.

Bond yields rise.

Fed rate-cut expectations disappear.

Rate-hike risk increases.

The dollar strengthens.

Gold falls.

That is the chain driving the market now.

The latest US employment data made that chain even stronger. The jobs report came in stronger than expected, reinforcing the idea that the US economy is still resilient enough to handle restrictive policy. Markets are now pricing roughly a 70% chance of a Fed rate hike in December, up from around 50% before the jobs report.

That is a major shift.

It means the market is no longer debating whether the Fed cuts this year. That trade is dead for now. The debate has moved to whether the Fed may need to tighten again if inflation keeps rising.

This is exactly why gold sold off.

Gold does not pay interest. So when the market prices higher policy rates and higher Treasury yields, the opportunity cost of holding gold increases. Investors can earn more from cash and bonds, while gold becomes less attractive unless fear becomes strong enough to overpower the rates channel.

Right now, fear is not overpowering rates.

The labour market is key here.

If jobs were weakening badly, the Fed would have a reason to look past some of the oil-driven inflation and focus on protecting growth. But strong employment data does the opposite. It gives the Fed room to stay restrictive.

That is why the combination of strong jobs and high oil is so bearish for gold.

Strong jobs reduce the urgency to cut.

High oil keeps inflation pressure alive.

Together, they keep the Fed hawkish.

This also explains why the dollar remains supported. Higher expected US rates make dollar assets more attractive, while Middle East uncertainty adds defensive demand. That creates a double headwind for gold because bullion is priced in dollars and tends to struggle when the dollar strengthens.

For yields, the pressure remains upward.

The market is demanding more compensation for inflation risk, especially because this inflation shock is coming from energy supply disruption rather than domestic demand alone. That makes it harder for the Fed to dismiss. If oil stays elevated, CPI, PPI and PCE remain vulnerable to further upside pressure.

For risk sentiment, the setup is also heavy.

Higher oil squeezes consumers and businesses. Higher yields raise discount rates. A Fed that may hike instead of cut tightens financial conditions. That is not a clean backdrop for equities, especially outside sectors with strong earnings momentum.

So the current picture is clear.

Gold is not falling because geopolitical risk has disappeared.

Gold is falling because geopolitical risk is inflationary.

The war is keeping oil elevated.

Oil is keeping inflation pressure alive.

Strong US jobs are giving the Fed room to stay tight.

Markets are pricing a higher chance of a December hike.

And that is pushing gold lower.

For gold to stabilize properly, the market needs one of two things.

Either oil needs to fall through real progress on Hormuz and the wider Middle East conflict, or US data needs to weaken enough to pull yields lower and reduce Fed hike risk.

Until then, gold remains vulnerable.

The key takeaway is simple.

Gold is not losing to peace.

Gold is losing to rates.