Gold is rising because the market is starting to unwind the inflation shock that has pressured bullion for months.

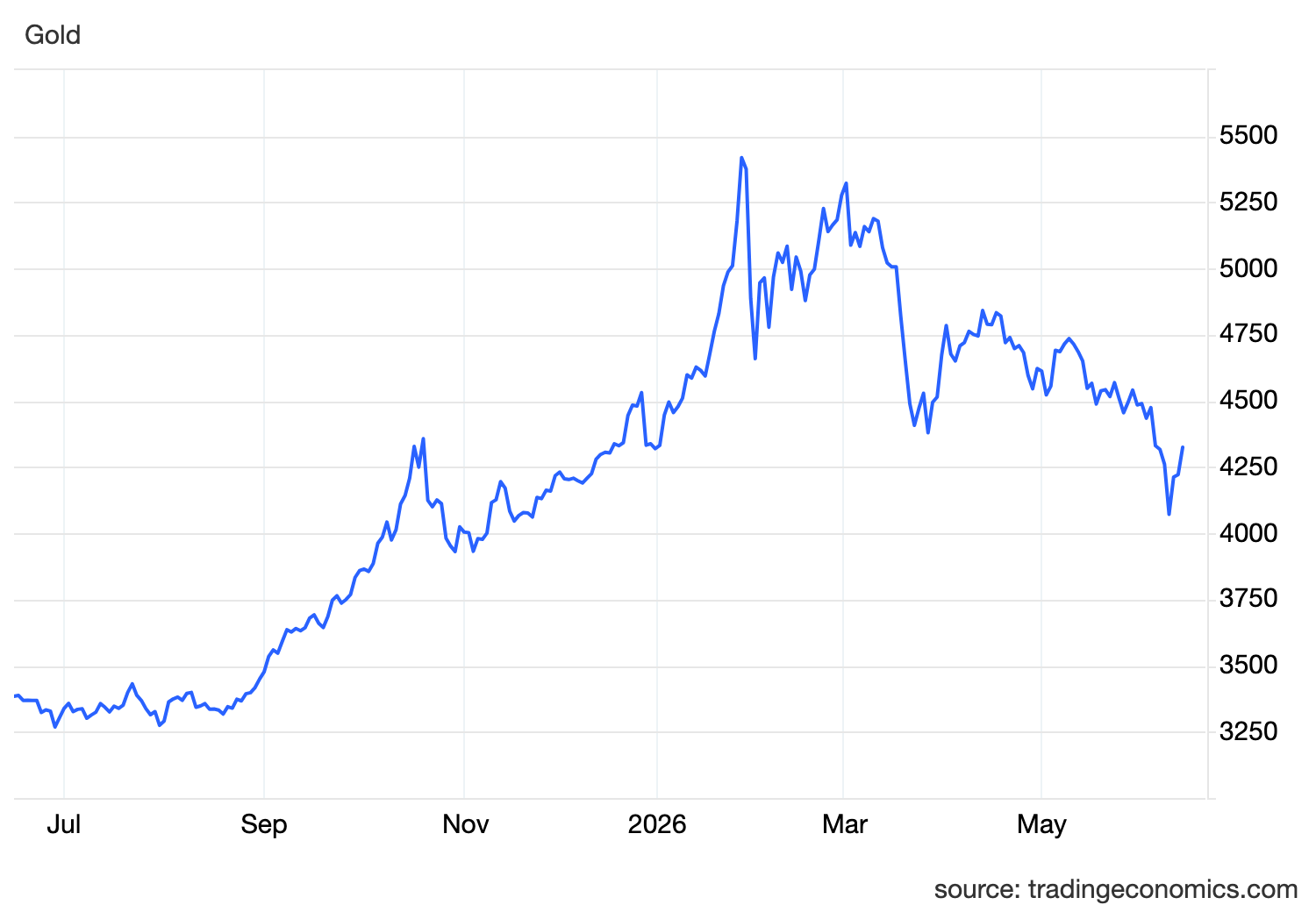

The metal climbed above 4300 for a third straight session after the US and Iran reached a peace agreement aimed at reopening the Strait of Hormuz. The deal is expected to be signed in Switzerland on June 19 and reportedly includes the lifting of blockades, sanctions relief for Iran and provisions tied to dismantling Tehran’s nuclear program.

The immediate market reaction came through oil.

Crude fell to a two-month low after the announcement, and that is the key reason gold is finding support. For most of this conflict, gold did not behave like a clean safe-haven asset because the war was not only creating uncertainty. It was also creating inflation.

The near-closure of Hormuz pushed oil higher, which lifted fuel costs, transport costs, import prices and production expenses. That pressure moved into inflation data and forced markets to price a more restrictive Federal Reserve. As yields rose and the dollar strengthened, gold came under heavy pressure because it does not pay interest.

Now that chain is beginning to reverse.

If Hormuz reopens, oil supply confidence improves. If oil keeps falling, inflation pressure eases. If inflation pressure eases, Treasury yields can cool. If yields cool, the opportunity cost of holding gold falls.

That is why gold can rise even as geopolitical fear fades.

This is the important distinction. Gold is not rising because the peace deal increases safe-haven demand. It is rising because the peace deal weakens the rates pressure that had been crushing bullion.

The Fed is central to this setup.

This week marks the first policy meeting under Kevin Warsh, with markets widely expecting rates to remain unchanged. The decision itself is not the main event. The guidance is. Investors want to know whether the Fed still sees inflation as dangerous enough to keep hike risk alive, or whether the oil collapse gives policymakers room to sound more balanced.

The Fed cannot turn dovish immediately. Inflation is still above target, and recent labour data has shown the US economy remains resilient. But lower oil changes the forward risk. It reduces the chance that the next inflation prints keep accelerating, and it weakens the argument for another rate hike before year-end.

That matters for gold.

Gold struggled when markets moved from rate-cut expectations to hike risk. If lower oil forces traders to reduce those hike bets, gold gets relief through lower yields and a softer dollar.

The dollar is already part of the story.

The peace deal reduces demand for the dollar as a safe-haven asset. It also lowers the inflation pressure that had kept US yields supported. A weaker dollar makes gold cheaper for foreign buyers, adding another layer of support to bullion.

The global central bank picture adds more nuance.

The Reserve Bank of Australia is expected to hold policy steady, reflecting a softer labour backdrop and a need to wait for more data. The Bank of England is also expected to hold, although inflation risks remain uncomfortable. The Bank of Japan is the outlier, with markets expecting a rate hike to support the yen and continue policy normalization.

That mix matters because gold trades against the global rates environment, not just the Fed.

If the Fed, RBA and BoE hold while oil falls, global rate pressure becomes less aggressive. But if the BoJ hikes, the yen may strengthen and the dollar could face more pressure, which would also support gold indirectly.

Still, this is not a risk-free gold rally.

The deal has to be signed. Hormuz has to reopen. Blockades have to be lifted. Shipping conditions have to normalize. If the agreement stalls or either side disputes the terms, oil can rebound quickly and bring the inflation problem back into the market.

That is the main risk.

For now, the market is pricing relief rather than full confirmation. Gold is recovering because traders see a credible path toward lower oil, lower inflation pressure and less Fed tightening risk. But a sustainable move higher depends on execution.

The current picture is clear.

Peace reduces safe-haven demand, which would normally be negative for gold. But in this cycle, the bigger driver has been rates. If peace lowers oil and oil lowers inflation, then yields can fall, the dollar can soften and gold can recover.

That is why gold is rising.

The war premium is coming out of oil.

The inflation premium is coming out of yields.

And the pressure on gold is finally easing.