Gold is falling because markets are treating the latest Middle East escalation as an inflation shock, not a simple safe-haven event.

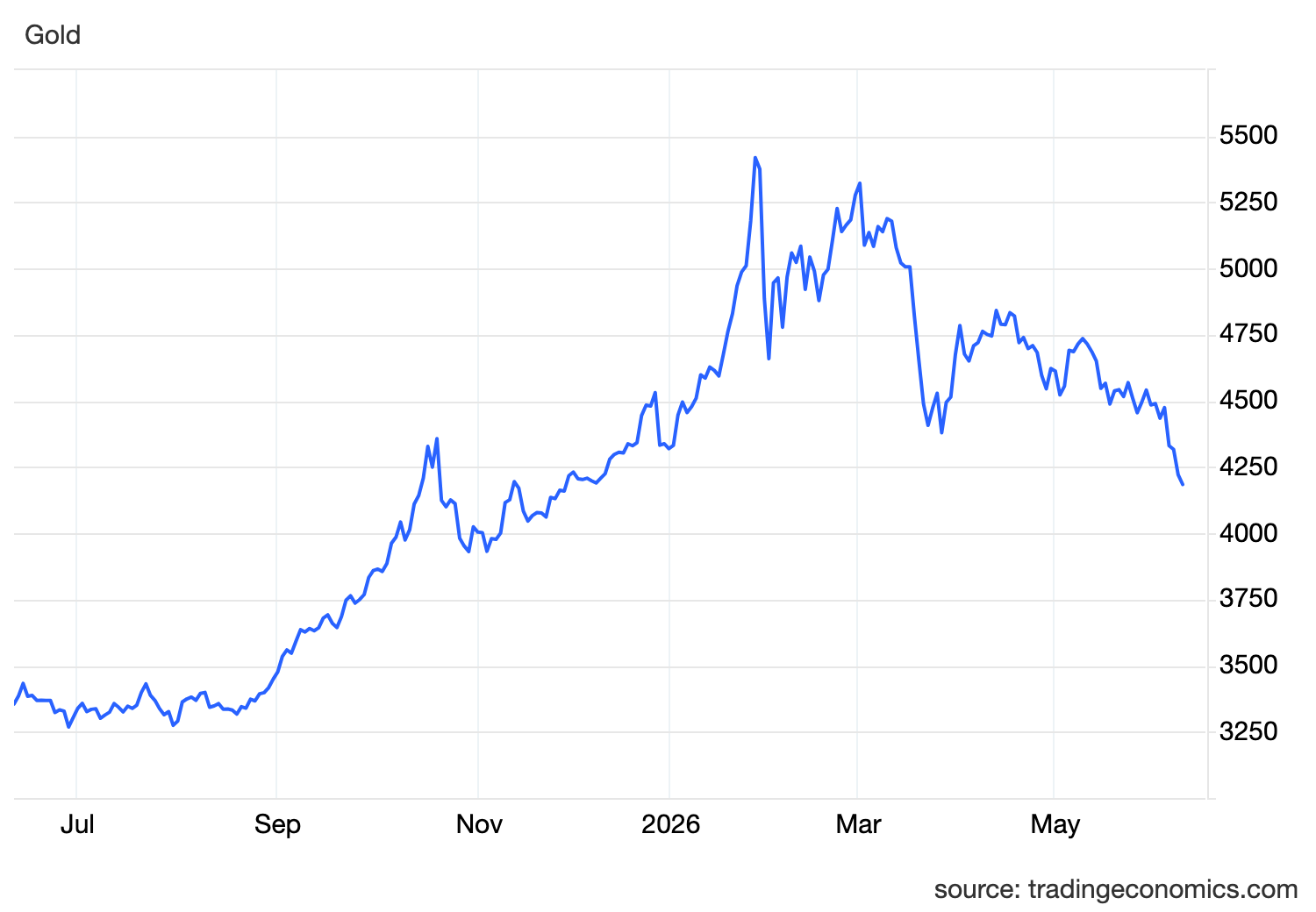

The metal dropped below 4200, reaching its lowest level since March 23, after the US launched new strikes against Iran following the downing of an American helicopter. In normal conditions, that kind of geopolitical escalation would be expected to support gold. This time, the reaction is different because the conflict is directly feeding into oil prices, inflation expectations and interest-rate pricing.

The key issue remains the Strait of Hormuz. The latest strikes have weakened confidence in the fragile ceasefire and raised doubts about whether a broader peace agreement is still achievable. As long as Hormuz remains near-closed, energy supply from the Persian Gulf remains constrained, shipping risk stays elevated and oil prices remain vulnerable to further spikes.

That is the pressure point for gold.

Higher oil does not stay inside the energy market. It feeds into fuel costs, transport costs, production expenses and import prices. Once that happens, inflation becomes harder for central banks to ignore. This is why the market is no longer looking at the war only through a defensive lens. It is looking at how the war affects inflation, yields and the Federal Reserve’s reaction function.

The transmission is clear. The escalation keeps Hormuz risk alive. Hormuz risk keeps oil elevated. Higher oil keeps inflation pressure in the system. Higher inflation pressure pushes Treasury yields higher. Higher yields increase the opportunity cost of holding gold.

That is why bullion is weakening even as geopolitical risk rises.

Gold does not pay interest. When investors can earn more from cash, bonds and dollar assets, gold becomes less attractive unless fear is strong enough to overpower the rates channel. Right now, the rates channel is still dominant.

The timing also matters because investors are waiting for fresh US inflation data. CPI and PPI will show whether the energy shock is still moving through the broader economy. If inflation comes in hot again, the Fed will have even less room to soften its stance. That would keep yields supported, strengthen the dollar and continue to pressure gold.

The labour market is another reason the Fed remains boxed in. Stronger-than-expected US employment data has already increased expectations that the Fed could raise rates before the end of the year. A resilient labour market gives policymakers room to stay restrictive because they do not need to rush to protect growth.

That combination is difficult for gold. Inflation risk is rising, the labour market is holding, the Fed can stay tight and markets can continue pricing hike risk. This is the same pattern that has defined gold’s weakness since the conflict began.

The dollar adds another layer of pressure. Higher US yields support demand for dollar assets, while geopolitical uncertainty also gives the currency a safe-haven bid. A stronger dollar makes gold more expensive for foreign buyers, reinforcing the downside pressure on bullion.

For risk assets, the same chain matters. Higher oil raises costs for consumers and businesses. Higher yields tighten financial conditions. A Fed that may hike instead of cut removes one of the major supports for equities. This is not only a gold story. It is a broader repricing of inflation and policy risk.

The current setup is straightforward. Gold is not falling because markets are calm. Gold is falling because the escalation is inflationary. The war is lifting oil, oil is lifting inflation expectations, inflation is lifting yields and yields are overpowering safe-haven demand.

Until oil cools, Hormuz reopens or US inflation data weakens enough to pull yields lower, gold remains vulnerable. War risk may create short-term bids, but as long as the conflict keeps feeding inflation, gold rallies are likely to struggle.