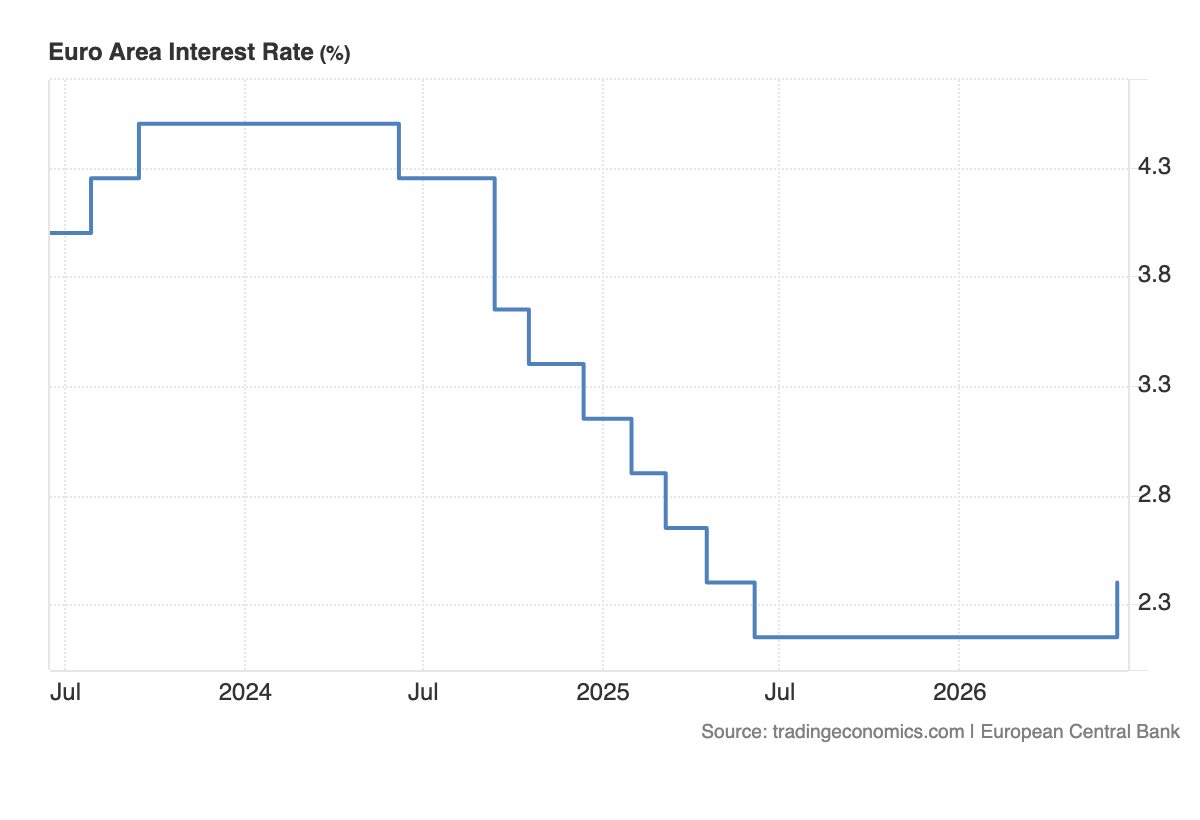

The ECB just made a clear statement: inflation credibility comes first, even when growth is slowing.

The European Central Bank raised interest rates by 25 basis points at its June meeting, marking its first rate increase since 2023. The decision was driven by a sharp change in the inflation outlook, with higher energy prices from the Iran conflict and disrupted oil shipments through the Strait of Hormuz feeding directly into the euro area’s price path.

This is not a normal inflation cycle.

The eurozone is not hiking because growth is booming. It is hiking because an external energy shock is threatening to keep inflation above target for longer. That distinction matters because it makes the policy trade-off harder. The ECB is tightening into a weaker growth outlook, not a stronger one.

The central bank raised its inflation forecasts materially. Headline inflation is now expected at 3.0% in 2026, up from 2.6%, and 2.3% in 2027, up from 2.0%. Core inflation was also revised higher to 2.5% for both 2026 and 2027. That tells markets the ECB is no longer treating the energy shock as isolated.

The concern is pass-through.

Higher oil prices first hit fuel and utility costs. Then they move into transport, food, goods and services. If firms begin passing higher input costs to consumers, and if workers begin demanding compensation for higher living costs, the energy shock becomes broader inflation. That is what the ECB is trying to prevent.

This is the reaction function.

If inflation expectations stay anchored, the ECB can move carefully. If inflation expectations begin to drift higher, the ECB has to tighten even if growth is weak. The rate hike is designed to signal that the central bank will not allow the war-driven energy shock to become embedded in wages, prices and long-term expectations.

The growth side is the problem.

The ECB lowered its GDP forecasts to 0.8% in 2026 and 1.2% in 2027. That means the eurozone is facing a difficult mix of higher inflation and weaker demand. Consumers are being squeezed by higher energy costs, businesses are facing higher input prices and confidence is being hurt by geopolitical uncertainty.

That is not a clean hiking environment.

It is a defensive hike.

The ECB is not tightening because the economy can easily absorb higher rates. It is tightening because the inflation risk has become too large to ignore. That is why this decision matters for markets. It shows that central banks are being forced to respond to oil-driven inflation even when growth momentum is fragile.

The comparison with the Federal Reserve is important.

The Fed is facing a similar inflation problem, with recent US CPI data showing renewed price acceleration due to energy costs. But the US economy still has a more resilient labour market, which gives the Fed more room to stay restrictive. Europe does not have the same growth cushion, which makes the ECB’s decision more delicate.

This creates a different kind of policy risk for the eurozone.

Higher rates can support the euro by improving rate differentials, especially if markets believe the ECB may need to continue tightening. But if investors focus more on weak growth, the euro may struggle to rally cleanly. A central bank hiking into soft growth is not automatically currency bullish.

For eurozone bond markets, the message is clearer.

Yields are likely to stay supported because inflation forecasts have been revised higher and the ECB has reopened the tightening cycle. Shorter-dated yields are especially sensitive because they reflect policy expectations. Longer-dated yields will depend on whether investors fear persistent inflation or weaker growth more.

For equities, the setup is mixed but uncomfortable.

Banks may benefit from higher rates, but higher borrowing costs pressure consumers, property, leveraged companies and rate-sensitive sectors. Energy-linked inflation also hurts margins, especially for firms that cannot pass on costs. If the ECB continues tightening while growth weakens, risk sentiment becomes harder to sustain.

For gold, the ECB decision reinforces the global rates pressure.

Gold has already been struggling because the Iran war has lifted oil, oil has lifted inflation and inflation has pushed central banks away from rate cuts. The ECB hike adds to that theme. When major central banks move toward tighter policy, global yields stay elevated and non-yielding assets like gold face pressure.

The key market point is simple.

The Iran conflict is no longer just a geopolitical story. It is a central-bank story.

Oil disruption through Hormuz has created an inflation shock. That inflation shock is forcing policy makers to defend credibility. The ECB has now joined the tightening side of that global response.

The next question is whether this becomes one hike or the beginning of a broader cycle.

If oil prices stabilize and inflation expectations remain anchored, the ECB can stop after a limited adjustment. If the conflict drags on, energy prices stay elevated and core inflation remains sticky, markets will price further hikes.

That is the risk now.

Europe is not dealing with strong growth and high inflation.

It is dealing with weak growth and imported inflation.

That is the worst kind of inflation for a central bank because it forces action without offering economic comfort.

The ECB has chosen credibility over patience.

Now markets have to decide whether that protects the eurozone from inflation, or pushes a weak economy closer to stagnation.