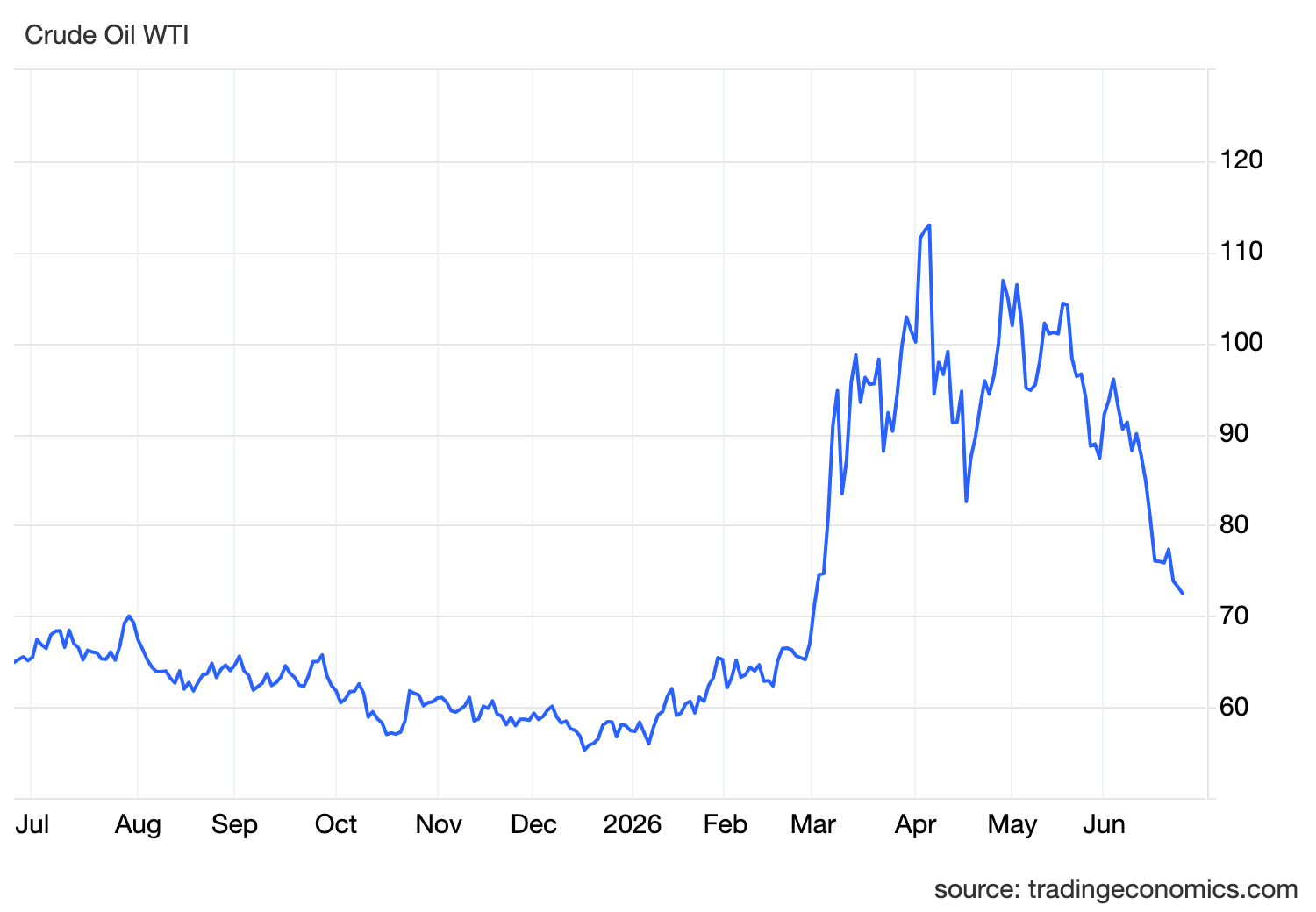

The oil market is rapidly pricing out the geopolitical premium that dominated much of the year.

WTI crude fell toward $72 per barrel, moving closer to levels seen before the outbreak of the Middle East conflict as supply conditions continued to improve across the Persian Gulf.

The latest decline reflects a market that is becoming increasingly confident that the worst of the energy disruption is over.

For months, the Strait of Hormuz sat at the center of global markets.

The disruption of shipping through the waterway removed millions of barrels per day from global energy flows, creating a supply shock that pushed oil above $110 per barrel at its peak. That surge became one of the primary drivers behind the global inflation resurgence seen throughout the second quarter.

The consequences extended well beyond oil.

Higher energy prices lifted transportation costs, manufacturing expenses and consumer fuel bills. Inflation accelerated across major economies, forcing central banks to reassess policy plans that had previously been moving toward stability.

The Federal Reserve became one of the clearest examples.

Last week, policymakers left rates unchanged but sharply raised inflation forecasts. PCE inflation projections were lifted from 2.7% to 3.6%, while roughly half of FOMC members signaled at least one additional rate hike could be necessary.

The inflation shock created by oil remains embedded in the data.

What is changing now is the outlook.

The market is increasingly focused on future supply rather than past disruptions.

That shift was reinforced this week by several important developments.

The International Maritime Organization reported receiving security assurances that could allow hundreds of vessels to safely transit the Strait of Hormuz. At the same time, efforts continue to evacuate stranded crews and normalize shipping operations throughout the region.

Meanwhile, the IEA reported that UAE exports have already recovered to roughly 85% of pre-conflict levels.

That figure is particularly important because it suggests producers are adapting faster than many expected.

Alternative pipelines, expanded storage capacity and rerouted shipments have allowed Gulf exporters to restore significant volumes even before a final peace agreement is reached.

The latest US decision adds another layer of supply.

Washington's new 60-day waiver allowing international buyers to purchase Iranian crude effectively accelerates the return of Iranian barrels to the global market. Combined with recovering exports from neighboring producers, the waiver significantly increases expectations that global supply balances will improve during the second half of the year.

This is why oil continues falling despite lingering geopolitical uncertainty.

Markets are looking ahead.

The focus is no longer on how much supply was lost.

The focus is on how much supply is returning.

That transition matters for inflation.

The energy shock that pushed US CPI to 4.2% and forced central banks into a more hawkish posture was largely driven by supply constraints. As those constraints ease, the inflation impulse that fueled higher yields and tighter policy expectations should gradually weaken.

That does not mean central banks will immediately change course.

The Federal Reserve has repeatedly emphasized that inflation remains too high. Officials will need several months of evidence showing lower energy costs filtering through the economy before becoming comfortable that inflation is moving sustainably lower.

However, falling oil changes the direction of risk.

A few months ago, markets were worried about worsening supply shortages.

Today, they are debating how quickly supply can normalize.

That is a very different conversation.

Treasury yields have already begun stabilizing after their sharp rise earlier in the quarter. Equity markets have welcomed lower energy costs as investors anticipate relief for consumers and businesses.

For global growth, the implications could be substantial.

The energy shock acted as a tax on economic activity. Lower oil prices reduce costs for households, improve profit margins for companies and support demand across energy-importing economies.

Asia stands out as one of the biggest beneficiaries.

Countries such as Japan, South Korea and India remain highly dependent on imported energy. A sustained decline in oil prices would ease inflation pressures and improve external balances throughout the region.

Still, one important uncertainty remains.

Iran and Oman have begun discussions on a framework for managing transit through Hormuz, including potential fee structures for vessels using the waterway.

While the proposal is still in its early stages, it highlights that the future of Hormuz may not simply return to the status quo that existed before the conflict.

Even if shipping resumes fully, the geopolitical landscape surrounding the strait may have permanently changed.

For markets, however, the bigger story remains supply.

Oil prices are falling because the market increasingly believes the supply shock is ending.

And if that view proves correct, the next major move may not be in oil itself.

It may be in inflation, yields and central bank expectations.