The Bank of Japan has taken another major step away from the ultra-low-rate era.

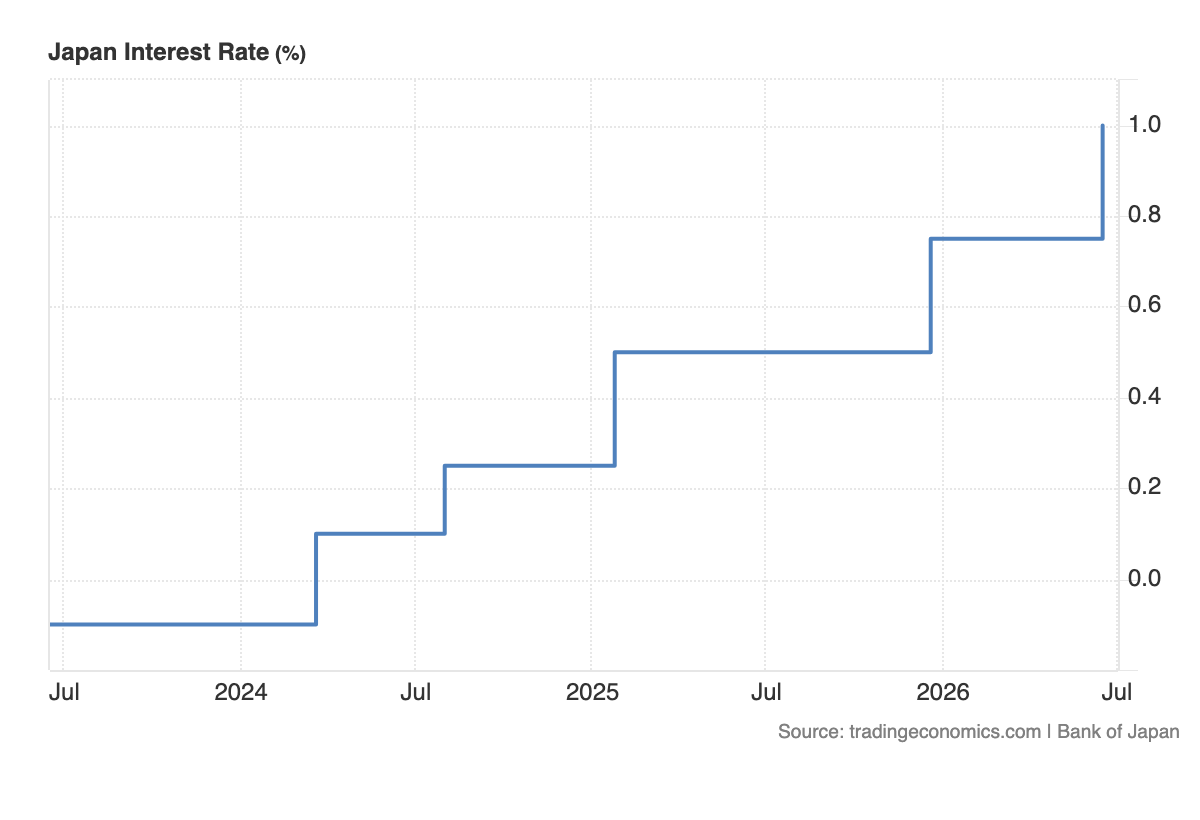

The central bank raised its short-term policy rate by 25 basis points to 1.0% at its June meeting, bringing borrowing costs to their highest level since September 1995. The decision was widely expected, but it is still a major signal. Japan is no longer treating inflation as temporary enough to justify emergency-level policy.

This hike is about inflation credibility, the yen and policy normalization.

For years, Japan’s problem was not too much inflation. It was too little inflation. That is why the BoJ kept rates extremely low for so long and even pushed policy below zero in 2016. The current setup is very different. Inflation pressure is now persistent enough that the central bank has to keep normalizing, even if growth is not booming.

The main driver is imported inflation.

Japan is highly exposed to energy prices because it imports most of its fuel. The Iran conflict and the disruption around the Strait of Hormuz pushed oil prices sharply higher in recent months, raising import costs, producer prices and household inflation pressure. Even though the US-Iran peace agreement has now pushed oil lower, the BoJ is still reacting to the inflation already moving through the economy.

That is important.

Central banks do not only respond to today’s oil price. They respond to the pass-through already embedded in wages, prices, business costs and inflation expectations. Japan’s producer prices have already accelerated sharply, showing that companies are facing higher input costs. If firms pass those costs to consumers, inflation becomes harder to contain.

The yen is the second major issue.

A weak yen makes imported energy and food more expensive. That worsens the inflation problem and hurts household purchasing power. By raising rates, the BoJ is trying to reduce pressure on the currency and narrow the gap between Japanese rates and the rest of the world.

But this is not simple.

The Federal Reserve is still expected to keep policy restrictive under Kevin Warsh, even as lower oil reduces some inflation pressure. If US yields stay high, the dollar can remain supported. That limits how much relief the yen gets from a BoJ hike unless Japanese policymakers signal that more tightening is coming.

So the market will care less about the hike itself and more about the guidance.

If the BoJ suggests that 1.0% is not the end of the cycle, Japanese yields can continue rising and the yen can strengthen. If the BoJ sounds cautious and signals patience, markets may treat the hike as already priced in, which could limit the yen’s recovery.

For Japanese bonds, this is a clear regime change.

A 1.0% policy rate means the floor under Japanese yields is higher than before. Investors now have to price a central bank that is no longer suppressing rates in the same way. That can keep JGB yields elevated, especially if inflation remains sticky or if markets expect another hike later this year.

The fiscal backdrop also matters.

Japan’s debt burden is high, and higher yields increase the cost of government financing. That creates a delicate balance for policymakers. The BoJ needs to defend inflation credibility, but aggressive tightening could raise debt-service concerns and put pressure on growth.

For equities, the message is mixed.

Banks can benefit from higher rates because lending margins improve when the yield curve moves higher. But exporters and growth stocks face a more complicated setup. A stronger yen can reduce overseas earnings when translated back into yen, while higher yields can pressure valuations, especially in technology and AI-linked names that have helped drive the Nikkei to record highs.

That does not mean Japanese equities are suddenly weak.

AI momentum remains powerful, and Japan is deeply tied into the global semiconductor and infrastructure supply chain. But the policy backdrop is becoming less friendly. The market now has to balance AI earnings strength against higher domestic rates and potential yen appreciation.

For global markets, the BoJ hike matters because Japan is a major capital allocator.

When Japanese yields were near zero, domestic investors had strong incentives to buy foreign bonds and overseas assets. As Japanese yields rise, some capital can become more attractive at home. That can affect global bond demand, currency flows and broader liquidity conditions.

This is why the BoJ is not just a Japan story.

It is part of the global repricing of central banks after the energy shock.

The Fed is trying to balance strong labour data against inflation risks. The ECB has already turned more hawkish because energy prices lifted its inflation forecasts. The BoJ is now hiking because imported inflation, yen weakness and producer-price pressure have made patience harder to justify.

The US-Iran peace deal may reduce future inflation pressure by lowering oil and reopening Hormuz, but it does not erase the inflation already created. That is why the BoJ still moved.

The current picture is clear.

Japan is normalizing policy because inflation pressure has become too persistent to ignore. Lower oil may reduce the urgency for aggressive follow-up hikes, but the central bank has already crossed a major threshold.

The key takeaway is simple.

The BoJ is no longer defending ultra-easy policy.

It is defending inflation credibility.