Australia’s labour market just delivered a clear warning.

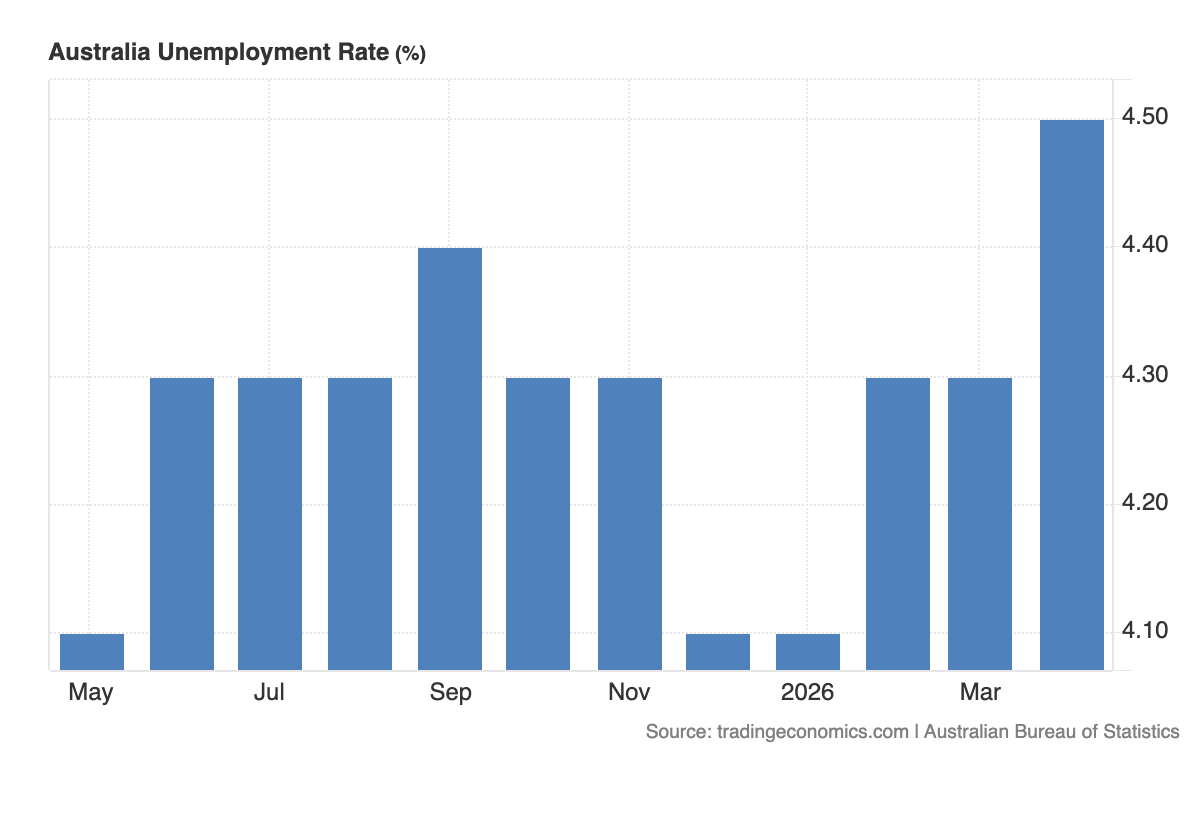

The unemployment rate rose to 4.5% in April, above expectations of 4.3% and the highest level since November 2021. Employment fell by 18,600, missing forecasts for a gain, while the number of unemployed people rose by 33,000 to 692,500. The participation rate also eased to 66.7%, showing that labour market momentum is starting to soften. The Australian Bureau of Statistics confirmed that employment declined and unemployment rose by 0.2 percentage points in seasonally adjusted terms.

This is not just a weak jobs print.

It changes the policy conversation.

Before this release, the Reserve Bank of Australia was dealing with a difficult inflation backdrop. Global energy prices had been rising because of the Middle East conflict and supply disruption around the Strait of Hormuz. For Australia, that matters because higher oil feeds into fuel costs, transport costs, business input costs and household inflation expectations.

That is the inflation side of the problem.

But now the labour market is giving the RBA a growth warning.

When unemployment rises and employment falls, the central bank has less room to tighten aggressively. Higher rates would risk deepening the labour slowdown, especially if households are already under pressure from higher borrowing costs and energy prices.

That is why markets cut expectations for another RBA hike after the data. Reuters reported that the chance of a June hike fell sharply after the unemployment rate hit 4.5%, while NAB pushed its expected next hike from June to August.

The key point is that this data does not make the RBA’s job easy.

It makes it harder.

If the inflation problem were fading, a weaker labour market would give the RBA a clean reason to pause. But inflation risk is still being fed by oil. The Middle East conflict has kept global energy prices elevated, and that pressure can move into Australia through petrol prices, freight, food distribution and business costs.

So the RBA is now facing a classic policy squeeze.

Inflation risk says stay hawkish.

Labour weakness says be careful.

That is the exact kind of setup where central banks prefer to wait for more data rather than move too quickly.

The details also matter.

Full-time employment fell sharply, which is more concerning than a decline driven only by part-time work. Full-time jobs are usually a better signal of underlying labour demand, so weakness there suggests firms may be becoming more cautious.

At the same time, hours worked increased by 16 million to 2.036 billion. That softens the signal slightly. It suggests employers may still be using existing workers more intensively, even as headline employment falls. So the labour market is weakening, but it has not collapsed.

That distinction matters for the Australian dollar.

A softer labour market reduces RBA hike expectations, which is normally negative for the currency. But the Aussie also trades as a global growth and commodity-linked currency. If oil remains high because of supply disruption, Australia may receive some terms-of-trade support through broader commodity pricing, but risk sentiment can still suffer if higher energy costs squeeze global growth.

Against the US dollar, the pressure is more direct.

The Federal Reserve is facing hot CPI and PPI readings after the same oil shock fed into US inflation. Markets have priced out Fed cuts and are even considering hike risk later this year. If the Fed remains more hawkish while the RBA becomes more cautious because of rising unemployment, the rate differential can work against the Australian dollar.

That is the cross-asset logic.

Weak Australian jobs lower RBA hike risk.

Hot US inflation keeps Fed policy tight.

That combination supports the US dollar over the Aussie.

For Australian bonds, the labour data should pull yields lower at the front end because it reduces near-term hike pressure. But longer yields may remain sensitive to global inflation and US Treasury moves. If oil keeps inflation expectations elevated globally, Australian yields may not fall cleanly.

For equities, the reaction is mixed.

A lower chance of RBA hikes helps rate-sensitive sectors because it reduces pressure from borrowing costs. But a weaker labour market also points to softer household demand. That can hurt consumer-facing companies if unemployment keeps rising.

So the current picture is not simple.

Australia’s labour market is weakening, and that reduces the case for immediate RBA tightening. But the global inflation backdrop has not disappeared because oil remains the key macro risk.

The RBA now has to decide which risk is more dangerous.

Move too early, and it may worsen the labour slowdown.

Wait too long, and oil-driven inflation may become embedded.

For now, the jobs data argues for patience.

But inflation still decides how comfortable that patience can be.