US yields are rising because the market is no longer debating when the Fed cuts.

It is now debating whether the Fed may need to hike again.

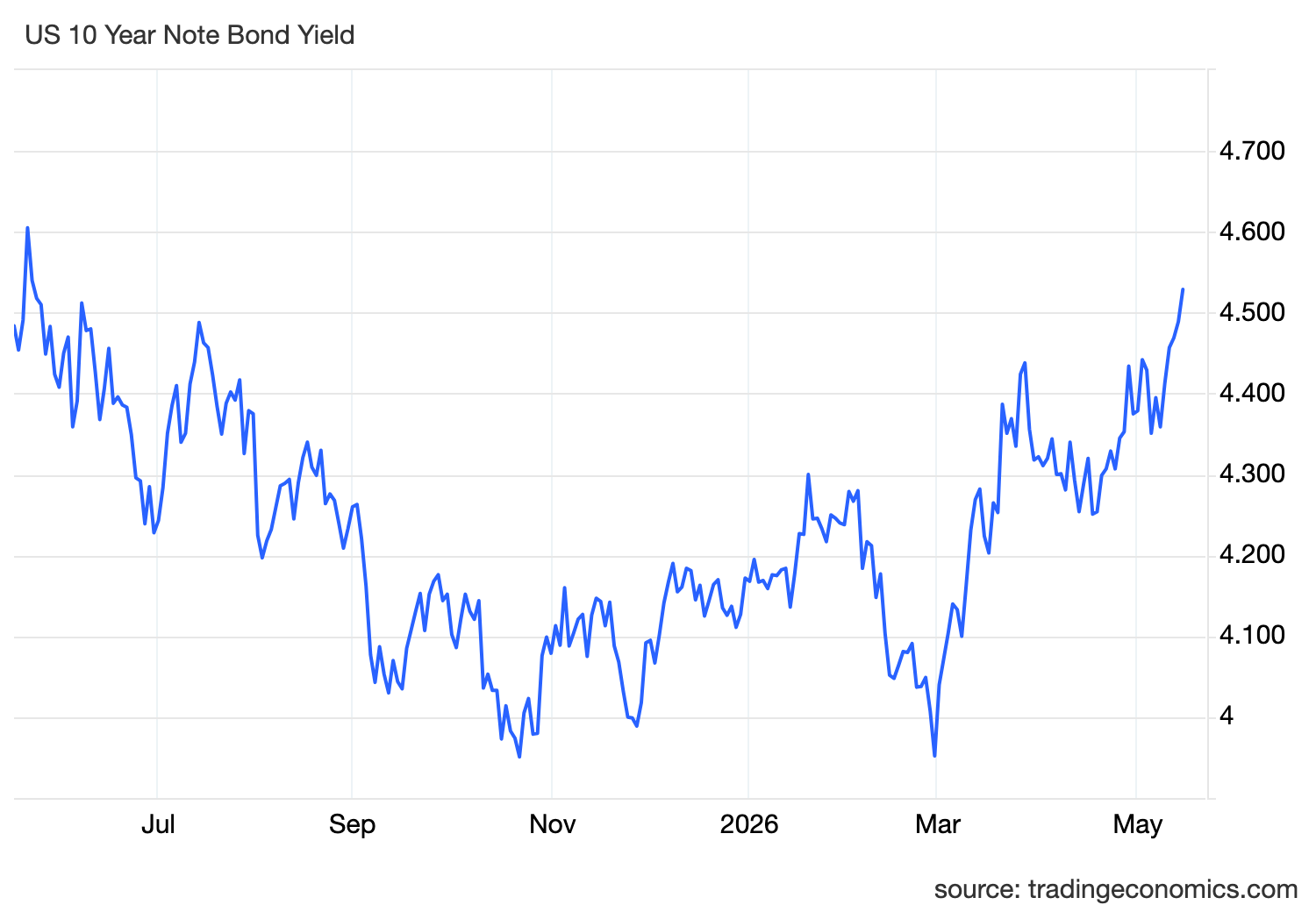

The yield on the US 10-year Treasury note climbed above 4.5% on Friday, reaching its highest level in a year as inflation pressure returned with force. The move was not random. It followed a week of data that confirmed one thing clearly.

The energy shock from the Iran war is now showing up in the inflation numbers.

Consumer inflation rose 3.8% in April, above expectations of 3.7%, marking the strongest annual increase since 2023. Reuters reported that the CPI rose 0.6% on the month, with energy goods accounting for more than 40% of the broad rise in inflation. That is the key detail. This is not just sticky inflation. This is oil-led inflation feeding through the economy.

Producer inflation then confirmed the same problem from the supply side. April PPI accelerated at its fastest pace since 2022, adding evidence that higher energy and input costs are moving through the business pipeline before they fully reach consumers. That matters because PPI is an early warning signal. If companies face higher costs, they either absorb margin pressure or pass those costs forward.

This is where the Iran war becomes a macro event, not just a geopolitical story.

The conflict has kept energy prices elevated by disrupting confidence around supply routes, especially through the Strait of Hormuz. When oil rises, it does not stay isolated inside the energy market. It raises transport costs, production costs, import costs and household fuel costs.

That creates the transmission chain markets are trading now.

Oil goes higher.

Inflation expectations rise.

Bond investors demand higher yields.

The Fed loses room to cut.

The dollar gets supported.

Gold becomes more complicated.

Risk assets face tighter financial conditions.

That is exactly why the 10-year yield is above 4.5%.

The bond market is not just reacting to one hot CPI print. It is reacting to the risk that inflation is becoming harder to bring down because the shock is external, persistent and energy-driven.

That matters for the Federal Reserve.

If inflation were rising while growth was collapsing, the Fed would have a painful trade-off. But the latest retail sales data shows the consumer is slowing, not breaking. April retail sales rose 0.5% from March, while spending excluding gasoline rose 0.3%, suggesting that higher fuel costs are eating into discretionary spending but have not destroyed demand yet.

That is the worst kind of setup for rate-cut hopes.

Growth is not weak enough to force the Fed into easing.

Inflation is too hot to allow the Fed to ease comfortably.

So policy stays restrictive.

Markets have now fully priced out the possibility of a Fed rate cut this year, while traders are increasingly assigning odds to a possible December hike. That repricing is what pushed yields higher. The market is no longer positioned for relief. It is positioned for the Fed to defend inflation credibility.

This is also why the dollar has a floor.

Higher US yields make dollar assets more attractive. At the same time, geopolitical uncertainty keeps some defensive demand in the currency. So the dollar is being supported by both rate differentials and safe-haven flows.

Gold is under pressure from the same mechanism.

Normally, war risk supports gold. But this war has repeatedly created the opposite problem. It pushes oil higher, which pushes inflation expectations higher, which pushes yields higher. Since gold does not pay interest, higher real yields raise the opportunity cost of holding it.

So gold can bounce on fear, but struggle when the rates channel dominates.

Risk sentiment also becomes more fragile.

Higher yields tighten financial conditions. Higher oil pressures consumers and margins. Sticky inflation reduces the probability of easier policy. That makes equities more sensitive to valuation pressure, especially if earnings momentum cannot offset the macro drag.

The Trump-Xi talks add another layer, but they are not the main driver yet.

Investors are watching the second day of high-level talks because trade policy can affect supply chains, tariffs and inflation. If trade tensions rise, markets may have to price another inflation channel on top of the oil shock. If talks ease tension, that could provide some relief to risk sentiment. But for now, the dominant force remains inflation and Fed repricing.

The current market picture is clear.

The oil shock is lifting CPI and PPI.

Hot inflation is pushing yields higher.

Higher yields are removing rate-cut expectations. And the Fed is now boxed in. Until oil cools or inflation data softens, the path of least resistance for yields remains higher, and the market will keep treating policy as tighter for longer.