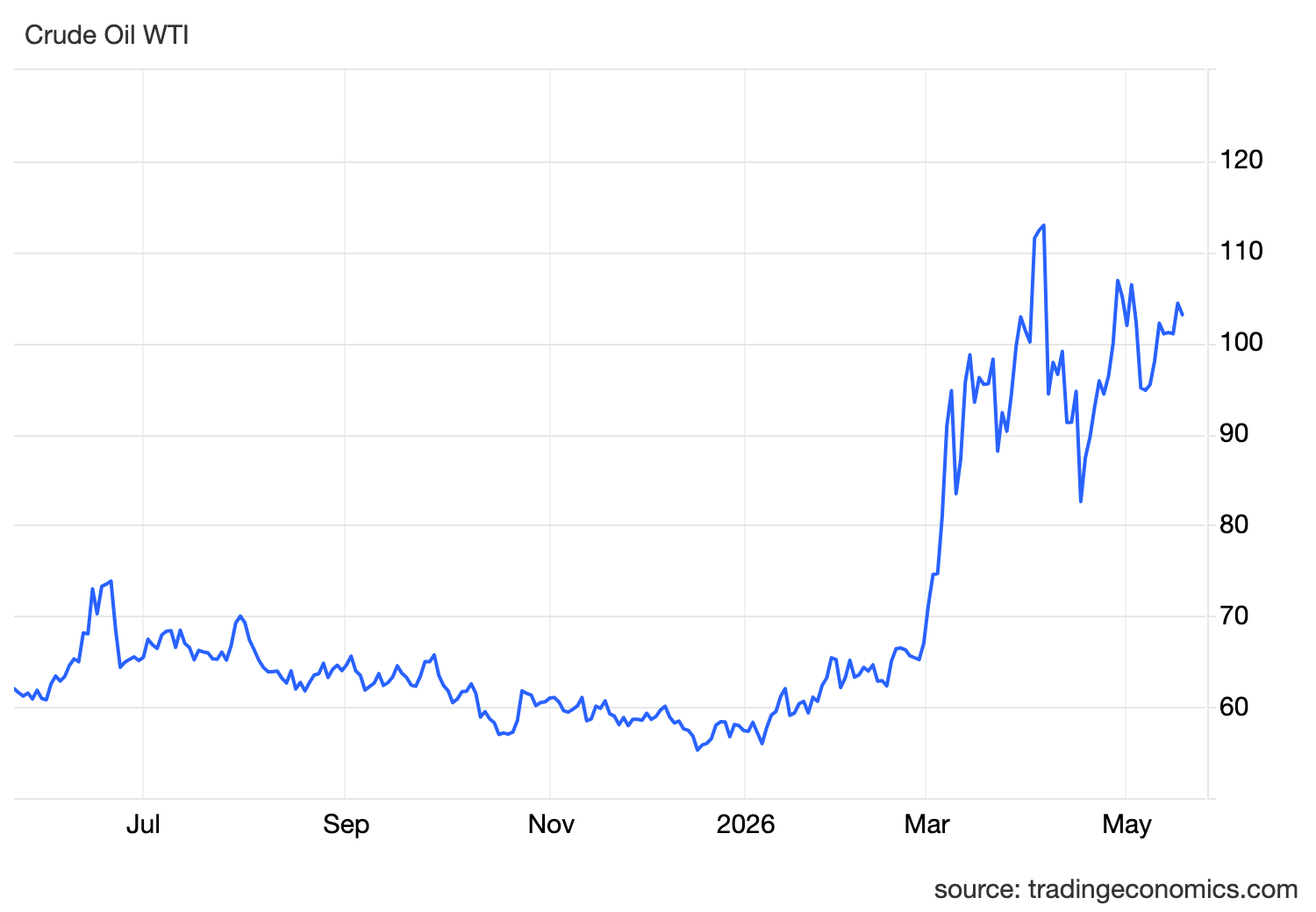

Oil is pulling back because the market has been handed a de-escalation headline.

WTI slipped toward 102 after President Trump said he called off a planned military strike on Iran following appeals from Saudi Arabia, Qatar and the UAE. The message from the Gulf was simple. Hold off, give diplomacy a chance, and avoid turning a fragile ceasefire into a wider regional shock. AP reported that Trump said serious negotiations were underway, although the market is still waiting for confirmation from Tehran.

That is why oil is giving back some recent gains.

When the probability of immediate military escalation falls, part of the war premium comes out of crude. Traders had spent more than a week bidding oil higher because US-Iran talks were stuck, Hormuz remained effectively closed, and the risk of a direct strike was rising. Removing the strike risk, even temporarily, gives the market a reason to breathe.

But this is not the same as saying oil risk is gone.

The key issue remains the Strait of Hormuz. The blockade and shipping disruption are still the central obstacles in negotiations, and Tehran’s nuclear program remains unresolved. Trading Economics also framed the move as oil slipping after Trump paused the strike, while noting that serious talks were claimed by Washington but not yet confirmed by Iran.

That distinction matters.

Oil is not falling because supply is normal again. It is falling because the worst-case escalation path has been delayed.

The physical market is still tight.

Reuters reported that oil prices dropped after Trump held off the planned attack, but the same report highlighted that traders remain focused on Iran’s response and the movement of tankers through the heavily affected Strait of Hormuz. It also noted that supply conditions remain sensitive, with crude reserve concerns and sanctions waivers still part of the broader energy picture.

The Russian crude waiver adds another layer.

The US allowing the sale of Russian crude and petroleum products already loaded onto tankers is effectively a pressure-release valve. It does not solve the Hormuz disruption, but it can soften near-term supply stress by preventing already-loaded barrels from being trapped in the system. That is bearish at the margin because it adds some immediate availability back into the market.

But again, it is not a structural fix.

The real question is whether Hormuz reopens properly.

If Hormuz remains constrained, oil stays vulnerable to another spike. If talks restart and shipping confidence improves, crude can continue giving back risk premium.

This is where the macro connection matters.

Oil has been one of the main reasons inflation risk has come back into focus. The Middle East conflict pushed energy prices higher, and that pressure has already started showing up in US inflation data. Recent CPI and PPI releases showed price pressure reaccelerating, forcing markets to price out rate cuts and reconsider the risk of a Fed hike later this year.

That is why every oil move now matters beyond energy.

When oil rises, inflation expectations rise.

When inflation expectations rise, Treasury yields rise.

When yields rise, the dollar gets supported.

When yields and the dollar rise, gold struggles.

And when energy costs stay high, risk assets face pressure through margins, consumers and tighter financial conditions.

This is the chain the market is trading.

Today’s oil pullback eases that pressure slightly. Lower oil reduces the immediate inflation impulse and gives bond markets a reason to stabilize. That can reduce some pressure on yields, soften the dollar at the margin, and give gold and equities room to recover.

But the relief is fragile.

The Fed cannot respond to one day of lower oil. It needs evidence that the energy shock is fading and that inflation pressure is cooling. Until then, policymakers stay cautious. Hot inflation data from last week already changed the policy conversation from rate cuts to higher-for-longer and possible hike risk.

So the current setup is not bearish oil in a clean way.

It is a pause in escalation.

Diplomacy has a window, but Tehran has not confirmed the talks. Hormuz remains the key blockage. The nuclear issue remains unresolved. And the Russian crude waiver only helps at the margin.

For the dollar, this reduces some safe-haven demand, but not enough to break the broader support if US yields remain elevated.

For gold, lower oil helps because it can reduce yield pressure, but if talks fail and crude rebounds, the rates channel comes back quickly.

For risk assets, the market can treat this as short-term relief, but not a full green light. A real risk-on move would require actual progress on Hormuz, not just a delayed strike.

So the takeaway is clean.

Oil slipped because Trump paused military action and diplomacy may restart.

But oil has not collapsed because the supply shock is not resolved.

Until Hormuz reopens and Iran confirms real negotiations, this is relief, not resolution.