Oil is rising because diplomacy is not delivering fast enough.

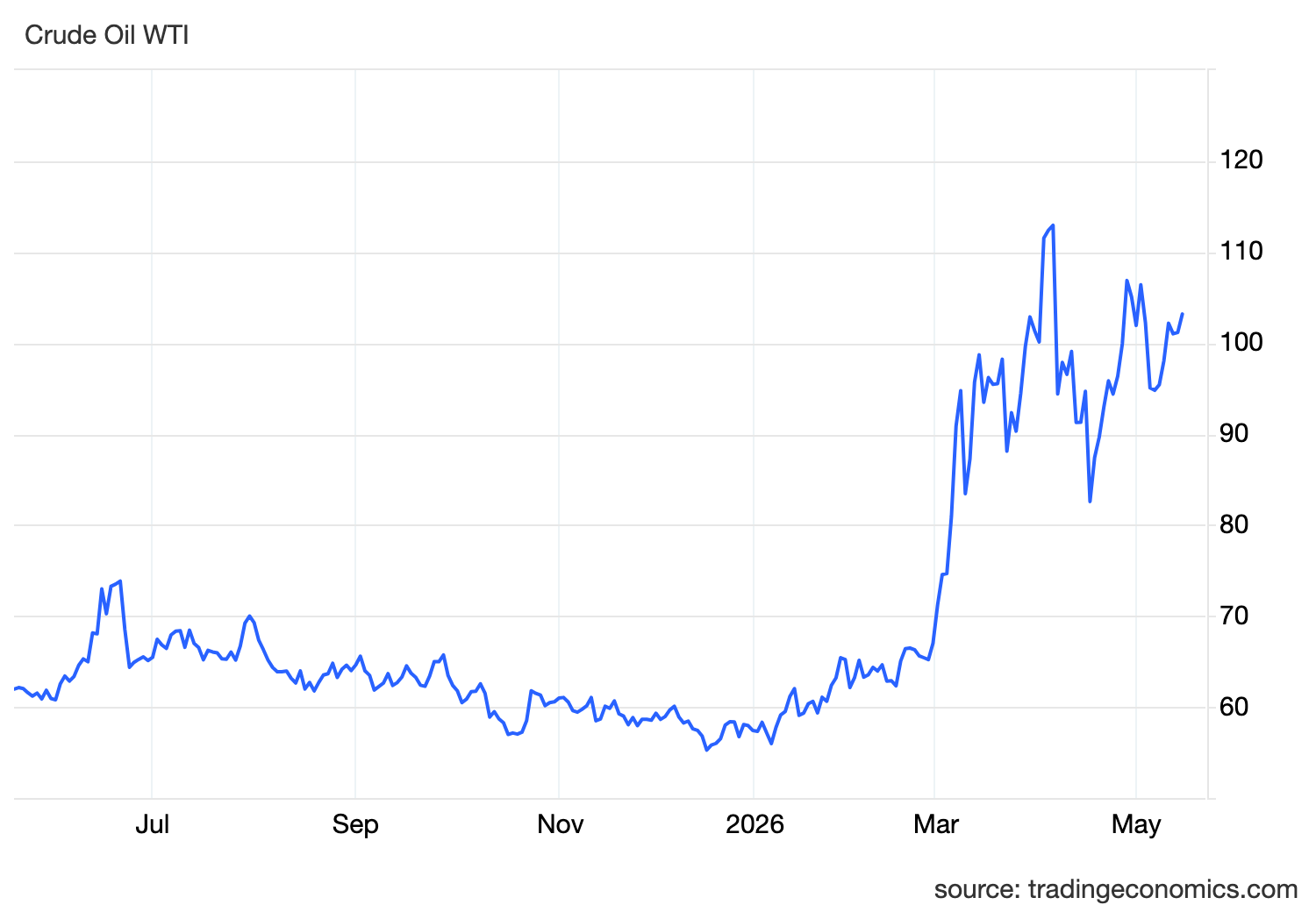

WTI crude moved above 102 and is on track for a weekly gain of more than 7%, as markets continue to price the risk that the Strait of Hormuz remains effectively closed for longer. The trigger is clear. Talks to end the US-Iran conflict are stalling, President Trump has described the ceasefire as being on “massive life support,” and Tehran’s latest response to the peace proposal has been dismissed.

That is enough to keep the oil risk premium alive.

But the real story is bigger than crude.

This is now a full macro shock.

The Strait of Hormuz is one of the most important oil routes in the world. When flows through that channel collapse, the market does not only lose barrels. It loses confidence in supply reliability. That forces traders, refiners, shippers and governments to price risk into every layer of the energy system.

The IEA’s latest numbers confirm how serious the disruption has become. It reported that global oil supply has fallen sharply since the conflict began, while flows through the Strait of Hormuz remain severely impaired. Reuters also reported that WTI rose more than 7% for the week, with continued ship seizures, attacks and weak ceasefire confidence keeping supply fears elevated.

That is why oil is not simply reacting to headlines.

It is reacting to a physical market that is tight.

The IEA has warned that the market could remain undersupplied through the third quarter even if the conflict starts to resolve soon. That is the key point. Even a political deal would not instantly repair shipping confidence, insurance conditions, routing schedules, inventories or refinery planning.

So the market is not just pricing today’s disruption.

It is pricing the lag.

That lag is what makes the inflation story dangerous.

Oil above 102 feeds directly into fuel, transport, production and import costs. The effect does not stop at petrol prices. It moves into freight, chemicals, food distribution, manufacturing inputs and consumer goods.

That transmission is already visible in the data.

US import prices jumped 1.9% in April, the biggest monthly increase in four years, driven by a 16.3% surge in imported fuel prices. That is a direct signal that the energy shock is moving into the broader price system.

CPI and PPI have also turned hotter.

US consumer inflation rose 3.8% in April, while wholesale inflation accelerated at its fastest pace since 2022. This is why markets have been repricing the Fed path. The issue is no longer whether inflation is sticky. The issue is that the oil shock is actively pushing inflation higher again.

That matters for yields.

When inflation risk rises, bond investors demand more compensation to hold long-term debt. That pushes Treasury yields higher. Higher yields then tighten financial conditions across the market.

This is the macro chain right now.

Oil rises.

Inflation expectations rise.

Treasury yields rise.

Fed cuts get priced out.

The dollar gets supported.

Gold struggles.

Risk assets face pressure.

That is why the oil rally matters for every asset class.

For the Federal Reserve, this is a difficult setup. If growth were collapsing, policymakers could look through some energy inflation and focus on supporting demand. But recent US data does not show a collapsing economy. Retail sales have slowed, but consumer spending remains resilient. Labour data has cooled, but it has not broken.

That gives the Fed room to stay restrictive.

And if oil keeps rising, it may force markets to keep pricing the risk of another hike later in the year.

That is the policy pressure oil is creating.

For the dollar, the setup remains supportive. Higher US yields attract capital, while geopolitical uncertainty adds defensive demand. Even when the dollar pulls back on peace headlines, the underlying support remains as long as oil keeps inflation alive and the Fed stays cautious.

For gold, the story stays conflicted. Normally, conflict risk should support bullion. But this war has repeatedly worked against gold through the inflation and rates channel. Higher oil lifts inflation, inflation lifts yields, and higher yields raise the opportunity cost of holding non-yielding gold.

So gold can bounce on fear, but it struggles when yields dominate.

For equities, oil above 102 is not clean. It raises company input costs, pressures consumers and reduces the chance of easier monetary policy. That is a tighter financial conditions story, not just an energy story.

The China angle also matters.

Trump’s comment that China wants to buy US oil shows how energy security is becoming part of the broader US-China discussion. China is a major energy importer, and with Hormuz still disrupted, Beijing has an incentive to diversify supply. For Washington, selling more oil to China could support US producers, but it also ties trade negotiations directly into the energy shock.

That means the Trump-Xi talks are not separate from the oil story.

They are part of it.

If China increases US oil purchases, that could help redirect some flows and reduce pressure at the margin. But it does not solve the bigger problem. The market still needs Hormuz to reopen properly for the supply risk premium to fade.

So the current picture is clear.

Oil is rallying because peace talks are stuck.

Hormuz remains effectively closed.

The physical market is undersupplied.

Inflation pressure is already showing up in US data.

Yields are rising because investors are demanding compensation for that inflation risk.

And the Fed is losing flexibility.

Until diplomacy produces a credible reopening of Hormuz, oil remains supported, inflation remains a market risk and the Fed stays trapped in a higher-for-longer framework.