Oil is climbing again because the market is losing confidence in a quick US-Iran deal.

WTI crude rose after President Donald Trump rejected Iran’s latest response to his proposal, reducing hopes that diplomacy could quickly reopen the Strait of Hormuz and stabilize crude flows.

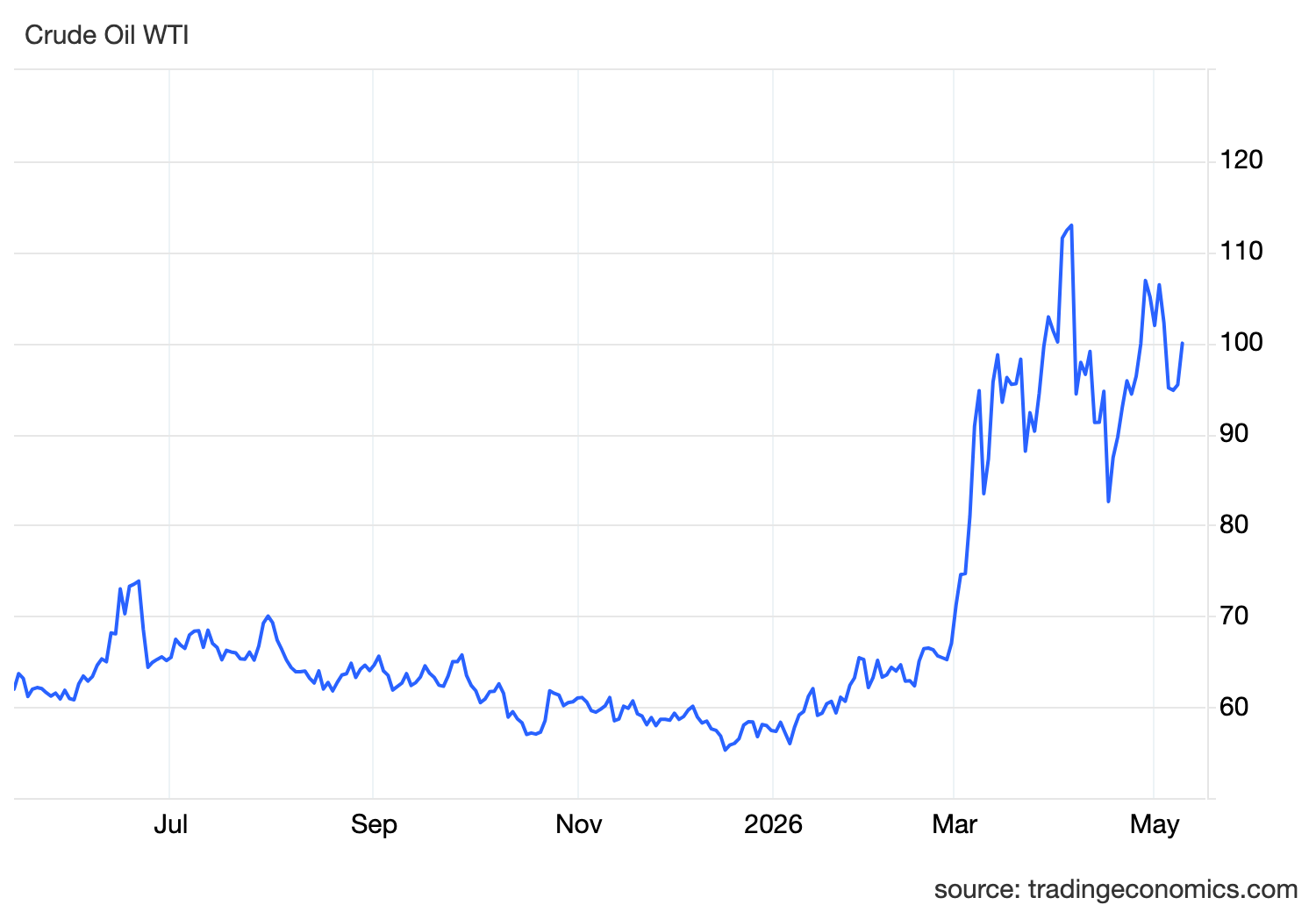

That matters because oil was coming off a weak week.

Prices had fallen as traders gave the ceasefire some room to hold and priced the possibility that negotiations could eventually reduce supply risk. But Trump’s rejection changes the tone. It does not completely kill diplomacy, but it delays the path to resolution.

And in oil markets, delays matter.

The Strait of Hormuz remains the central risk. If flows through the strait stay disrupted, the market cannot fully price normalization. Even if crude is not exploding higher every day, the risk premium remains embedded because one of the world’s most important energy routes is still vulnerable.

This is why the move in oil is more than a technical rebound.

It reflects a shift back toward supply risk.

The market is now balancing two forces.

The first is diplomacy. If talks restart and Iran moves toward a workable agreement, oil can give back some of the risk premium.

The second is escalation. If negotiations stall and both sides harden their positions, traders have to price a longer disruption to crude flows.

Right now, the second force is gaining weight again.

That has direct macro consequences.

Higher oil feeds into inflation expectations. Once energy prices rise, the pressure moves through transport costs, production costs and consumer prices. That makes inflation harder for central banks to ignore.

This is where the Federal Reserve comes in.

The Fed can stay patient when inflation is cooling and growth is slowing gradually. But if oil starts pushing inflation higher again, the Fed loses flexibility. Rate cuts become harder to justify, and markets begin to price a longer period of restrictive policy.

That supports yields.

Higher yields usually support the dollar, especially when US policy remains tighter than other major economies. The dollar can also benefit from safe-haven demand if geopolitical uncertainty rises again.

For gold, the picture becomes more complicated.

Geopolitical risk can support gold in the short term, but if oil lifts inflation expectations and pushes yields higher, gold can struggle. That is exactly why gold has been trading inconsistently through this conflict. Fear supports it, but rates limit it.

For risk assets, higher oil is not friendly.

It raises input costs, pressures consumers and tightens financial conditions through higher yields. Equities can absorb that for a while if growth remains strong, but a persistent energy shock eventually becomes a margin and valuation problem.

So the setup is clear.

Oil is not just reacting to headlines.

It is repricing the probability that diplomacy fails to quickly restore supply confidence.

If talks regain momentum, oil can cool and inflation pressure can ease.

If talks stall, Hormuz risk stays alive, oil remains supported and central banks stay constrained.

The key takeaway is simple.

Oil is climbing because peace hopes faded.

And if oil keeps climbing, the inflation story comes straight back into the market.