apan’s inflation problem is moving upstream again.

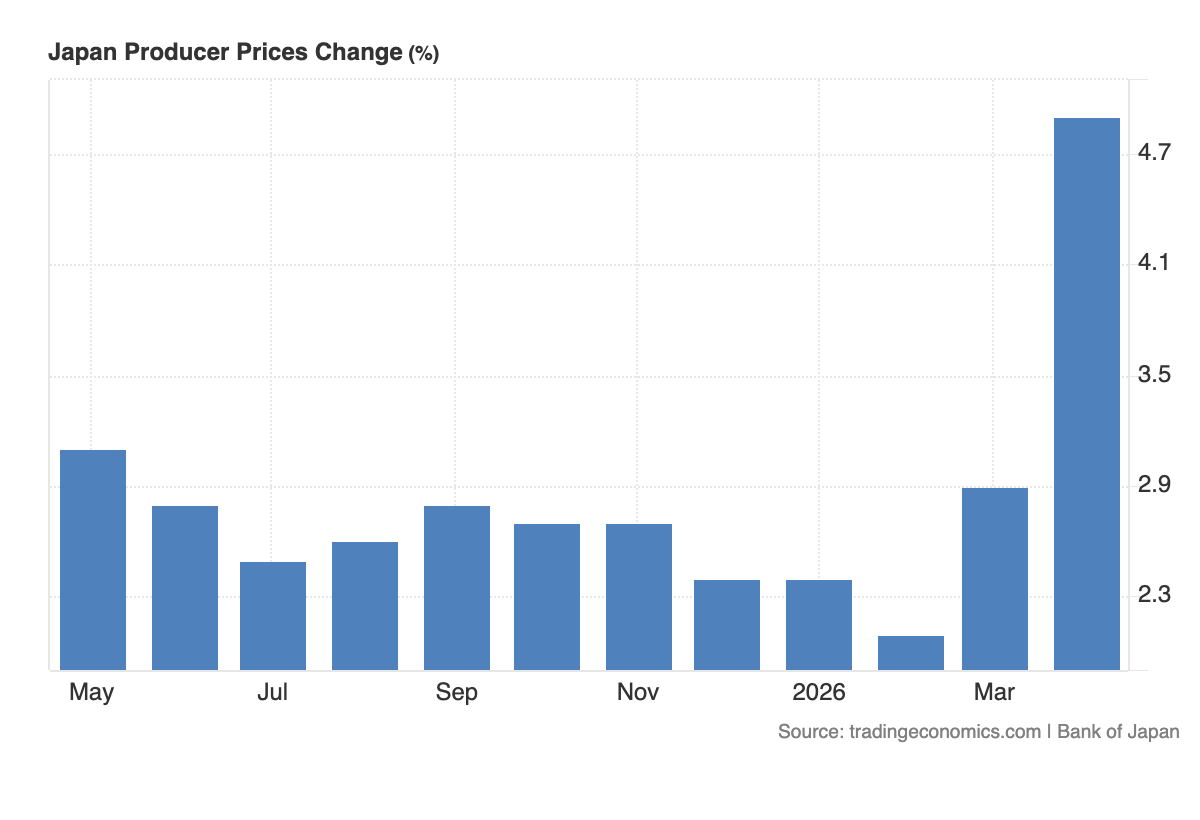

Producer prices rose 4.9% from a year earlier in April, well above expectations of 3% and sharply faster than the revised 2.9% increase in March. On a monthly basis, prices jumped 2.3%, the strongest monthly rise since April 2014.

That matters because producer prices are not just another inflation print.

They show what companies are paying and charging before those costs fully reach consumers. When wholesale prices rise this quickly, businesses face a choice. They either absorb the cost through weaker margins or pass it on through higher retail prices.

Neither outcome is clean for Japan.

The main driver is the energy shock from the Iran war. Disruptions around Middle East supply routes, especially the Strait of Hormuz, have pushed crude and fuel costs higher. For Japan, that matters more than it does for many other major economies because Japan is highly dependent on imported energy.

The Bank of Japan already warned in its April outlook that higher crude oil prices linked to the Middle East situation would hurt Japan through weaker corporate profits, lower household real income and a deterioration in the terms of trade. It also projected core inflation in the 2.5% to 3.0% range for FY2026 as oil pushes up energy and goods prices.

Now the producer price data is confirming that pressure.

The strongest signals came from areas directly tied to energy and industrial input costs. Chemicals rose 9.2%, petroleum and coal products swung to a 5.3% increase after falling in March, and electrical machinery, electronic components and transport equipment also accelerated. This tells us the shock is not limited to fuel. It is moving through Japan’s manufacturing base.

That is the key macro point.

Oil is no longer just lifting headline inflation. It is raising business costs across the supply chain.

This is exactly the kind of inflation the BoJ does not want.

Japan has spent years trying to generate durable demand-led inflation supported by wages and domestic consumption. But this is different. This is cost-push inflation driven by imported energy, weaker terms of trade and supply disruption.

That creates a policy trap.

If the BoJ does nothing, higher import costs can keep inflation expectations elevated and pressure the yen. A weaker yen then makes imported energy even more expensive, which feeds the same cycle again.

But if the BoJ tightens too aggressively, it risks hitting growth and household demand at the exact moment real incomes are already being squeezed by higher prices.

That is why this print is so important.

It strengthens the case for another rate hike, possibly as soon as the next policy meeting, but it does not make the decision easy. Reuters reported that the data has increased speculation around a June BoJ hike, especially as wholesale inflation broadened and import prices in yen terms surged.

The yen is central here.

A stronger BoJ tightening signal can support the yen by narrowing the gap between Japanese and US rates. But the global backdrop still matters. US inflation has also reaccelerated because of the same oil shock, with hotter CPI and PPI forcing markets to price out Fed cuts and keep US yields elevated.

That keeps the dollar supported.

So even if the BoJ turns more hawkish, yen strength may be limited if US yields stay high. This is the policy divergence problem Japan keeps running into. The BoJ is under pressure to normalize, but the Fed is also being held restrictive by inflation.

For Japanese equities, the message is mixed.

AI-linked and exporter-heavy stocks can still benefit from global tech demand and a weaker yen. But higher input costs are a margin problem. If companies cannot pass through the rise in energy, chemicals and transport costs, earnings pressure builds.

For Japanese bonds, this is clearly uncomfortable.

A hotter PPI print raises the risk that the BoJ has to tighten sooner. That puts upward pressure on Japanese government bond yields, especially if markets start believing inflation is becoming broader and less temporary.

For global markets, the lesson is simple.

The Iran war is not staying inside oil markets.

It is moving into inflation data.

Japan’s PPI is the latest proof. The same energy shock that is lifting US CPI and PPI is now hitting Japanese wholesale prices, forcing markets to reassess how much room central banks really have to ease.

The current picture is clear.

Oil is driving input costs higher.

Input costs are lifting producer inflation.

Producer inflation increases pass-through risk to consumers.

That pressures the BoJ to hike.

But because the inflation is imported and energy-led, tighter policy comes with real growth risk.

That is the difficult balance Japan now faces.

This is not healthy inflation.

It is imported cost pressure with policy consequences.