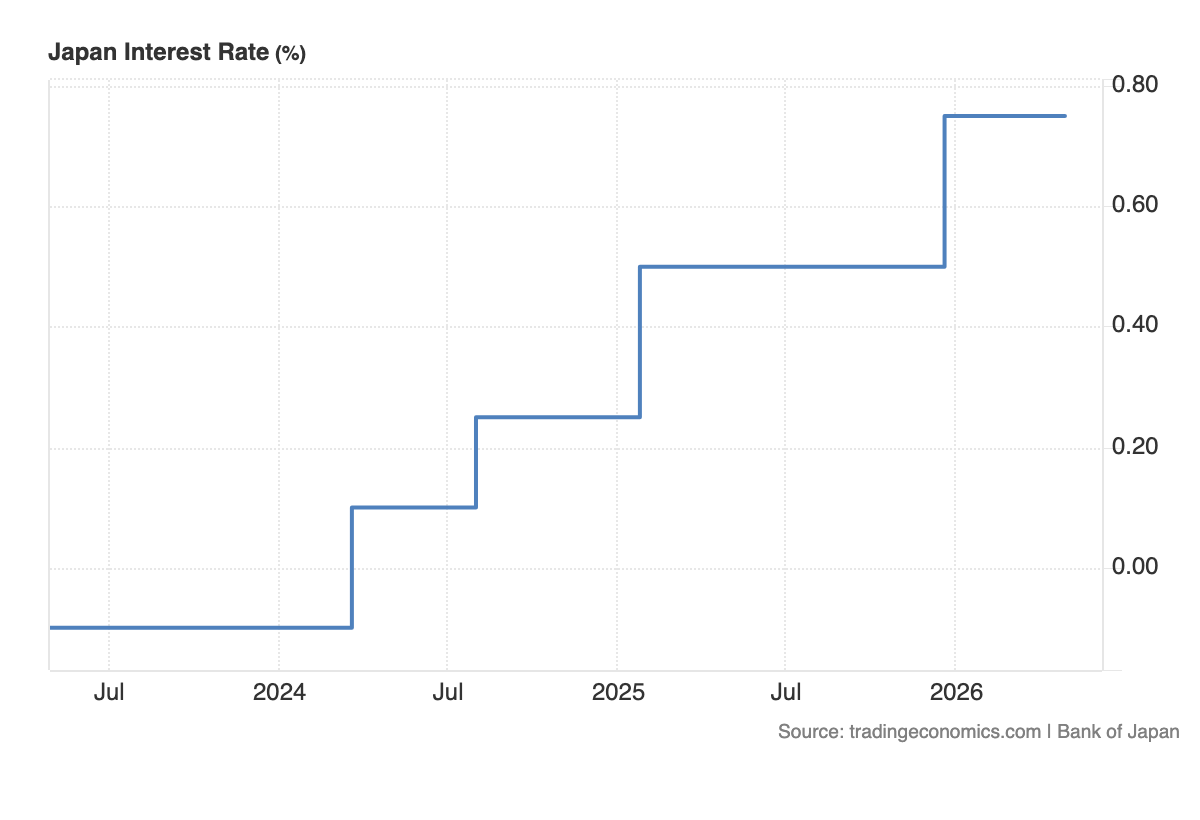

The Bank of Japan did not move, but the signal is clear.

Holding rates at 0.75% keeps policy at its highest level in decades, but the real story is in the split and the forecasts. A 6–3 vote shows that pressure to tighten further is building, even as growth weakens.

This is not a normal cycle.

Inflation is being driven higher by external forces, mainly energy. Rising oil prices are feeding into goods and consumer costs, forcing the BoJ to revise its inflation outlook sharply higher to 2.8% for FY2026.

At the same time, growth is losing momentum.

The downgrade in GDP to 0.5% reflects a softer domestic backdrop. Consumption is not accelerating enough, and external demand remains uncertain. Even though corporate profits and government support are providing some stability, the underlying trend is slowing.

This creates a difficult policy setup.

Higher inflation would normally justify tightening. But weaker growth limits how aggressively the BoJ can move. That tension is exactly what the dissenting votes are highlighting. Some policymakers want to move rates higher now, while the majority is choosing to wait.

That tells you where policy is heading.

The BoJ is shifting toward a tightening bias, but it is not ready to commit fully.

From a market perspective, this matters for the yen.

Higher inflation and a gradual move away from ultra-loose policy should support the currency over time. But as long as growth remains weak and global uncertainty stays elevated, the pace of tightening will be slow.

That keeps policy divergence in play.

The Federal Reserve is holding at restrictive levels. The BoJ is only just normalizing. That gap still matters for flows and for currency positioning.

So the bigger picture is clear.

Japan is entering a phase where inflation is rising without strong growth to support it. That limits policy flexibility and forces the central bank into a cautious, gradual path.

Filed under